Budget 2024: Ways To Save Capital Gain Taxes On Real Estate Gains (54EC Bonds)

Search for a command to run...

No comments yet. Be the first to comment.

In this series, we cover all instruments, schemes and products in the alternative investment space available for Indian retail investors.

KEY TAKEAWAYS FAAB Invest is launching FarmFraX, a fractional ownership model for agricultural land, offering investors rental income and potential capital gains. The model provides detailed information about the land, including topography, soil, a...

Many of you might have invested in Reliance Industries, TCS, HDFC Bank, SBI, or Infosys. After all, these are amongst the biggest companies in India which are listed on the stock market, so you can co

Real estate has traditionally been a “high-ticket” asset class. Either having lakhs (or even crores) of Rupees in your bank account or taking a huge home loan were the only two prominent ways to buy property. But that is changing now with fractional ...

India’s Finance Minister Nirmala Sitharaman is set to present the Union Budget this week on February 1st, 11 am. This will be her ninth consecutive Budget presentation, which brings her closer to former Finance Minister Morarji Desai’s record of pres...

Imagine you are an absolute equity lover. Stocks are your thrill ride, while debt funds are just a sleepy side note in your portfolio. But what if I told you there were years when those ‘boring’ debt funds left the stock market in the dust? And not j...

Can I ask you a question? Don’t worry, it's not a complex mathematical problem. Just a simple one- Whenever the stock market feels noisy and makes your portfolio bleed red, what’s the one thing you secretly wish for? I am sure it must be about having...

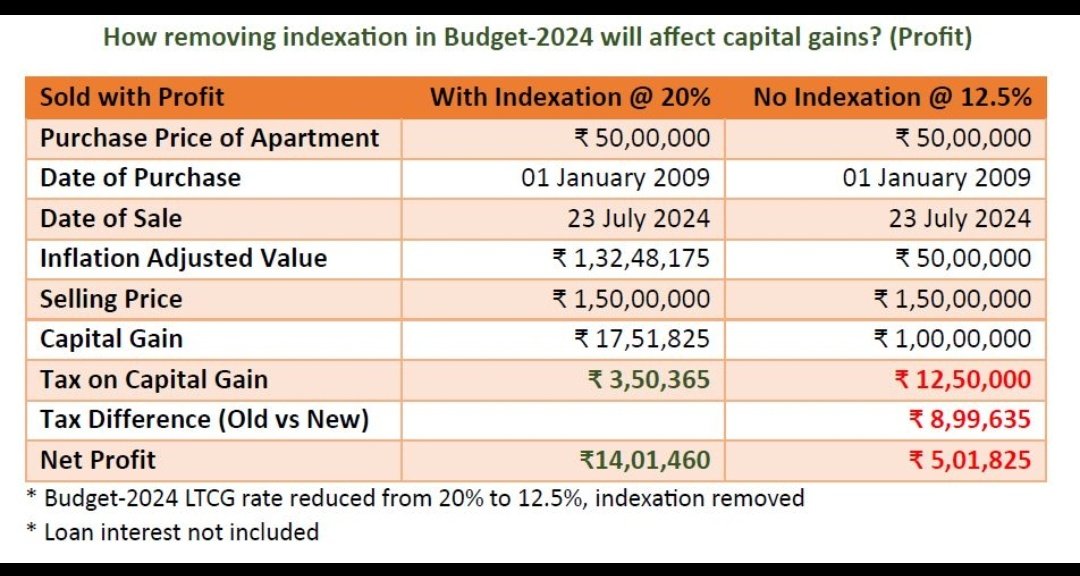

The Union Budget 2024 reduced the capital gains tax rate on real estate from 20% to 12.5% but removed the indexation benefit for properties purchased after 2001, causing dissatisfaction among investors.

To reduce capital gains tax liability, individuals can consider property renovations, buying another residential property under Section 54, or investing in 54EC Bonds.

Section 54EC Bonds allow taxpayers to invest capital gains from the sale of land or buildings to avoid paying taxes, with conditions such as a 5-year lock-in period and a maximum investment of ₹50,00,000.

54EC Bonds are issued by government-backed entities like REC Limited, PFC Limited, NHAI Limited, and IRFC Limited, offering interest rates between 5% and 5.25%.

While 54EC Bonds provide tax exemptions and are AAA-rated, they have limitations such as lack of liquidity and applicability only to gains from real estate sales.

In the Union Budget 2024, our honorable Finance Minister announced an increase in capital gains taxes for most investment avenues. However, for real estate, the tax rate was reduced from 20% to 12.5%, but with a catch. The government removed the indexation benefit for all homes purchased after 2001.

How do you think people reacted? Here's how:

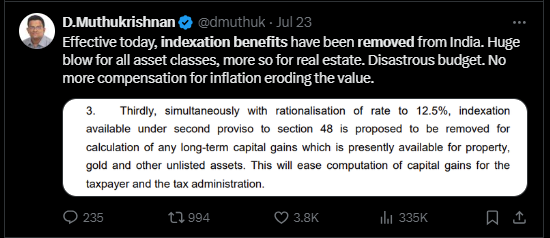

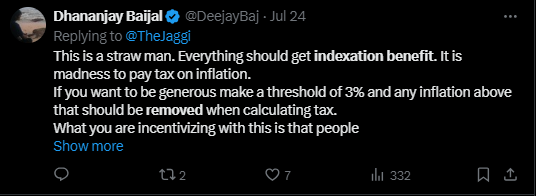

Needless to say, the participants in the Personal Finance Group of the ALT Investor Community were not happy with this move. Everyone wants to make money in property, but now the government wants us to pay tax on inflation, which feels unfair. Below is the significant difference in taxation that investors will face so the pain/anger is justified.

Source: This Tweet

A lot of people have problem with this new rule, but then whenever I have such problems in my life, I go back to this slide by Gaur Gopal Das.

Question is "Can You Do Something About It?"

NO. Then Why Worry?

If the answer is YES, then also why worry? Just Do It.

Sorry for getting all philosophical, but in this article, we will give you some tips on how you can practically save some capital gain taxes when you sell your next house/property with a special focus on 54EC Bonds (also known as Capital Gain Bonds)

Just to clarify, we will only cover the LTCG (Long Term Capital Gains) in this section assuming you have kept the property for at least for 24 months.

Here are some very simple practical things you can do to reduce your capital gains tax liability:

If, after purchasing your property, you made modifications that changed its floor plan and increased its value, you can add these renovation costs to your base price. When you sell the property, you deduct the buying price + renovation costs to determine the amount on which you have to pay capital gains taxes. For example, if you own a bungalow and you added another floor, increasing its market value, you can include the cost incurred in adding that extra floor. There are various exceptions to this rule so please consult a professional.

If you are an individual or HUF entity selling your existing residential property to buy another residential property within 1-year before or 2-years after the sale or even construct a new one within 3-years will be qualified for exemption of capital gain taxes. This is covered under Section 54 of the Income Tax Act and is widely known in the industry.

An example of this will be, you bought a house for INR 2 Crores and sold it for INR 6 Crores, making INR 4 Crores as Profit. If you then buy a new residential house for INR 6 Crores within the designated time frame. You pay zero capital gain taxes.

Section 54EC of Income Tax Act states that where a taxpayer earns capital gains from sale of land/building/house (not just residential property), they shall be exempted from payment of tax on such income if they invest an amount equivalent to the capital gain in 54EC Bonds within a period of 6 months from the date of sale.

Conditions

The minimum and maximum investment allowed is ₹20,000 and ₹50,00,000.

Investment to be made within 6 months from the date of sale.

Lock-in period of 5 years from the date of allotment. No sale or pledge of 54EC bonds is allowed.

If any condition is violated, the capital gain exempted shall be taxed as income in the year of violation.

54EC Bonds can be issued by the following companies, they all are Government Backed, AAA rated entities.

Rural Electrification Corporation Limited (REC Limited)

Power Finance Corporation Limited (PFC Limited)

National Highway Authority of India Limited (NHAI Limited)

Indian Railway Finance Corporation Limited (IRFC Limited)

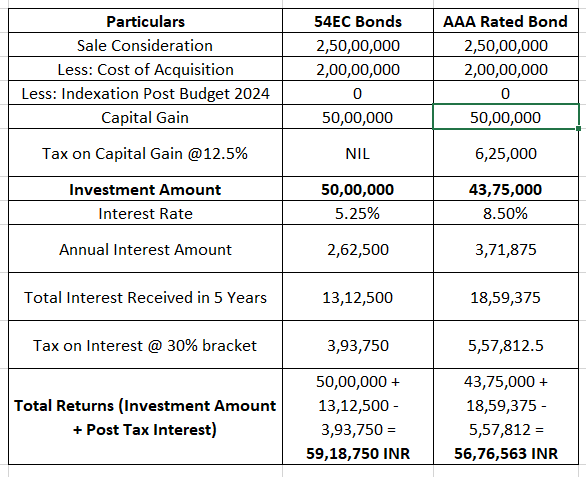

A Practical Example: You purchased a piece of land for INR 50 Lakhs in 2020. 4 years later, you managed to sell the land for INR 80 Lakhs making a handsome INR 30 Lakhs gain. You can either pay taxes on it at 12.5% interest rate without any indexation benefits (ouch) or you can invest in 54EC bonds and yield anywhere between 5% - 5.25% interest p.a.

As of 25 July 2024, unfortunately none of the OBP platforms offer these bonds. This is maybe because the issuer themselves sell these bonds via their portal or via debt brokers like SBI Securities. The commissions might also not be very lucrative for these OBP platforms to sell these bonds.

For making an bond offer to the public at large, the issuer is required to comply with the SEBI (Listing Obligations and Disclosure Requirements), 2015.

| Interest Rate | 5.00% - 5.25% |

| Mode of Issuance | DEMAT or Physical Form |

| Transferrable | Non-Transferable, Non-Marketable |

| Investment multiple | 10000 |

If you wish to apply in any of the bonds, here are links to their websites

I am 100% sure you must be thinking that isn't 5% - 5.25% very less as compared to other AAA issues in the market, yes they are and the govt has strategically kept it low since you are also taking the advantage of zero capital gains on sale of property.

Let's do a quick comparison, if you reinvest the profits in AAA Rated Bond instead of 54EC Bonds. The table assumes a minimum 5 Year Holding period which is a requirement for 54EC Bonds.

Even if you receive lower interest than a comparable AAA rated bond, you still make more money when investing in 54EC Bonds. Interesting Right?

Exemption - Investing in 54EC bonds after selling an immovable property helps save on long-term capital gains tax from the sale.

Credit Rated - These bonds are AAA-rated by independent credit rating agencies, and the issuers are public sector undertakings backed by the government.

No TDS - No TDS is deducted on the interest payments from 54EC bonds, so you have more money to reinvest or utilize.

NRIs Can Invest - For unknown reasons, NRIs cannot invest in a lot of debt products in India, fortunately 54EC is not one of them. If you sell a property and have NRI status, you can still invest in 54EC Bonds.

Capital Gain Exemptions From Sale of Limited Assets: The exemption from capital gains by investing in 54EC is only available if these are long term gains from sale of land/property. You cannot invest the gains of equities/Mutual Funds and then invest in these bonds to get an exemption. Do not do that.

In conclusion, while the recent changes in the Union Budget 2024 have made it more challenging to save on capital gains taxes from real estate, there are still viable strategies available. By considering renovations, understanding the implications of inherited property, reinvesting in another residential property, or investing in 54EC Bonds, you can effectively manage and reduce your tax liabilities.

Each method has its own set of conditions and benefits, so it's crucial to evaluate which option best suits your financial situation. Always consult with a tax professional to ensure compliance and optimize your tax-saving strategies.

Remember, if you can do something about it, why worry?

That's it for this article, thank you so much for reading, if you would like to join our community and the Personal Finance Discussion group within it, join here today!

Please note that this is an opinion blog and not official research advice. I am not a registered RIA in India, and none of these views reflect those of my current employer. This blog aims to promote informed decision-making and does not discourage you from investing in any deals.

We plan to come up with more blogs discussing different types of instruments available in the world of startup investing, write on due diligence for some platforms, and also existing and upcoming alt investment deals in the Indian market. If you want to stay updated on the latest blogs, please subscribe to our newsletter so you get notified automatically.

Thank you for reading and hope to see you in the next one!