Is India Tourism Here to Stay or Just a Passing Trend? The OYO Rooms Story!

Search for a command to run...

No comments yet. Be the first to comment.

ALTShares is a knowledge series powered by InCred Money. With ALTShares, we aim to explain the benefits and risks of investing in Pre-IPO Shares or Unlisted Shares as an alternative investment option.

KEY TAKEAWAYS The article explores the investment potential in Chennai Super Kings (CSK) through unlisted shares, highlighting the financial structure and revenue sources of the Indian Premier League (IPL). It details the revenue streams for IPL, i...

Many of you might have invested in Reliance Industries, TCS, HDFC Bank, SBI, or Infosys. After all, these are amongst the biggest companies in India which are listed on the stock market, so you can co

Real estate has traditionally been a “high-ticket” asset class. Either having lakhs (or even crores) of Rupees in your bank account or taking a huge home loan were the only two prominent ways to buy property. But that is changing now with fractional ...

India’s Finance Minister Nirmala Sitharaman is set to present the Union Budget this week on February 1st, 11 am. This will be her ninth consecutive Budget presentation, which brings her closer to former Finance Minister Morarji Desai’s record of pres...

Imagine you are an absolute equity lover. Stocks are your thrill ride, while debt funds are just a sleepy side note in your portfolio. But what if I told you there were years when those ‘boring’ debt funds left the stock market in the dust? And not j...

Can I ask you a question? Don’t worry, it's not a complex mathematical problem. Just a simple one- Whenever the stock market feels noisy and makes your portfolio bleed red, what’s the one thing you secretly wish for? I am sure it must be about having...

I am a CFA and FRM Charterholder. I used to work as a Portfolio Implementation Manager for Aviva Investors managing £3bn+in Assets Under Management in the UK. I am very passionate about educating people on how they can make more money with their existing investments sustainably.

The article discusses the growth and consolidation of the tourism sector in India, highlighting the importance of market share for investors, particularly in the hospitality sector with a focus on OYO Rooms.

It explains the dynamics of the hotel industry in India, noting the shift towards premium hotels and the increasing demand for luxury rooms, while also identifying a gap in the economy segment where players like OYO and Treebo compete.

OYO Rooms is no less than a turnaround story, having shifted from a loss-making model to profitability by focusing on the budget segment, cutting costs, and expanding internationally, particularly in Europe and Southeast Asia.

The article outlines OYO's business model, revenue sources, and cost structures, emphasizing its asset-light approach and improved financial performance, including positive EBITDA margins and net profit.

It concludes with an analysis of OYO's future outlook, fundraising plans, and valuation challenges, suggesting that OYO's growth potential in the unlisted shares market could be an attractive investment opportunity.

One common aspect that every great investor highlights about their investment picks is market share. Many top asset managers advise investing in companies that are either market leaders (proven monopolies) or are about to become market leaders (emerging monopolies).

A similar market consolidation is happening in the ever-growing tourism sector in India. The unlisted markets may offer retail investors a chance to get a piece of the action. In today’s article, we will cover the two core sectors in the tourism space where the top unlisted players are making significant moves.

This article is a part of our new series called ALTShares powered by InCred Money where we discuss unlisted shares and some specific sectors and opportunities in the unlisted shares space.

In this specific article, we will discuss the Hospitality Sector in detail and talk about OYO Rooms in the Unlisted Shares space, so stay tuned till the end of this article.

The Post-COVID travel excitement is real. Look around, and you'll see people have been travelling extensively after being stuck at home. You probably took a great trip with your family recently, maybe this summer or sometime not too long ago.

When you think about the tourism supply chain, it includes various entities like hotels, flights, trains, taxis, and tourist attractions. All of these have dynamic pricing and are operated by different companies. When tourism thrives in a country, these companies can offer unique and potentially lucrative investment opportunities.

However, it is difficult to pick the right stocks, as many external factors influence the earnings of these companies. For example, COVID-19, crude prices, corporate bookings, regulations, and sometimes even the weather can have an impact.

In India, the listed tourism space mainly comprises three sectors:

Transportation (Indigo, GMR Airports, IRCTC, etc)

Hotels (Samhi Hotels, IHCL, Lemon Tree, etc)

Online Travel Agents (OTAs) (Yatra, Thomas Cook, etc)

The hotel occupancy rates have returned to 66%, reaching pre-COVID levels, and have started to exceed the 70% mark, which is a historic high!

This situation will lead players to reinvest more cash into the business to increase the number of operational rooms. Any company investing cash at higher ROCEs for capacity addition will benefit in the long run due to this surge in demand.

(Source - Link) (Please zoom in to see the chart)

If we look closer (page 16 of this report), in the past year, the biggest increase in room supply was seen in cities like Dehradun, Jaipur, Udaipur, and Ahmedabad, which are known for attracting tourists from around the world. This increase in supply highlights how tourism drives the growing demand for hotels.

Some of the tailwinds that seem to be driving this tourism growth are vacationing and pilgrimage. According to the Indian Tourism report, which is published by the government each year - roughly 37% of tourists come to India for Leisure/Holiday purposes, while 21% come to visit temples, religious and cultural sites. 10% for business related work, and surprisingly 7% of tourists also come for medical reasons.

The micro picture of hotels in India is generally divided into two parts. Analysts separate hotel revenues, foot traffic, and earning trends by geography and the 'premiumness' of the hotel.

Currently, the industry is slowly shifting towards more premium hotels, as the demand for luxury rooms is very high. If we look at the market share of rooms with an Average Daily Rate (ADR) of ₹7,000-₹10,000, it has increased significantly in the past two years (almost 3 times). The same is true for rooms between ₹5,000-₹7,500 (1.7 times). Meanwhile, the share of low-cost rooms (less than ₹5,000) has decreased quite a bit. This shows a shift towards premium, upscale hotels.

(Source - Link)

Similarly, if we look at the geographical distribution of hotels, tourist destinations have seen a significant increase in rooms, while major corporate centers like Bangalore and Hyderabad are driving growth.

Another important point is the distribution of Upper Midmarket and Upscale rooms, priced between ₹7,500-₹15,000. Almost 50% of new capacity will be added in this price range, highlighting the growing demand and competition in the premium segment.

The overall increase in hotel capacity by 2028 is expected to be around 50%, and these are just conservative estimates.

Hotel Industry in India is dominated by 3 kinds of players.

The Hotel Real Estate Players - They partner with brands like Marriott and Hyatt to open hotels. They own the land and building, and manage daily operations. However, Marriott and Hyatt handle marketing, booking, and customer relations. Examples include Samhi Hotels and Juniper Hotels.

Hotel Player/Owners - These companies own or lease the property and manage daily operations, bookings, and marketing. Examples include Tata, IHCL, EIH, ITC, and Lemon Tree.

Hotel Aggregators - This model is similar to franchising but not exactly the same. These players provide branding, accessories, merchandise, and tech support to hotel owners. The owner refurbishes the place according to the aggregator's guidelines and gets listed on their app. The aggregator manages revenue collection, customer relations, and marketing. Companies like OYO and Treebo use this model.

The current market share of hotel sector in India looks something like this:

Even though there are many local mom-and-pop hotels, we can see that market share consolidation at the top has already begun. Marriott, Taj, Fern, ITC, Accor, and Hyatt control more than 50% of the market.

Now that we understand the hotel sector in India, let's look at OYO Rooms (Oravel Stays Pvt. Ltd.) and why it may be a good opportunity to invest in this unlisted share via InCred Money.

As more top players shift their focus towards the premium/upper-scale segment, a gap is left in the market for economy hotels. This is where companies like OYO are busy gaining market share and catering to the budget segment. Let's explore how OYO is achieving this and whether its finances can support its journey to becoming one of the leading hotel companies in the country.

OYO (Oravel Stays Limited) is a hotel aggregator/chain that works similarly to a franchise model. The key difference is that in franchising, franchisees pay a royalty to the brand, while here, OYO collects the revenues and pays a percentage to the hotel owner, similar to a marketplace model. Oyo records its GMV as a revenue and lease rentals/payments to hotel owners as its operating expense.

While earlier OYO used to lease hotel rooms earlier and used to give minimum guarantees to partner hotels, it has discontinued this model. The beauty of the current franchisee model is the asset light balance sheet. Where top Indian hotel players have to load their balance sheet with large properties and leverage it to achieve growth, OYO can do so without the need of large capital. We will understand how this may help the company in future but lets understand in what segment OYO operates first.

OYO currently caters to the budget/economy segment, generally in the ₹1000-₹4000 range. It has 18,000 hotels listed on its app, which are broadly split into three categories:

Premium Hotels - (₹2,500/ Night) (~15%)

(OYO Townhouse, Capital O, Silver Key, Home etc.)

Mid-range hotels - (₹1,500 - ₹2,500/Night) (~25%)

(OYO Capital O, Collection O)

Affordable stays - (₹1,500/ Night) (~60%)

(OYO Spot on, Rooms, Flagship)

It is important to note that OYO earns over 70% of its total revenue from overseas locations like the US, Europe, and Asia through their homestay and hotel business. Oyo’s homestay business in Europe is one of the largest in size, which has been fueled with acquisition sprees. As of 2024 it has -

85K homestays across European countries with a Fixed Fee + Commission Model

73K homestay listings on a subscription platform with a Fixed Fee Model

Till date, OYO has acquired around 13 companies in total, mostly in European regions such as Denmark, Belgium, Germany, France, Croatia and other nordic countries.

Big names such as Checkmyguest (Acquired for - $27.4Mn - Paris), Directbooker (Acquired for - $5.5Mn - Croatia), Leisure Group (Acquired for - $415Mn - Amsterdam) are now part of Oyo’s house of brands in Europe. All these companies had their own house of brands, hotel/homestay network, corporate clients and agent network (Similar to what Oyo has in India), which enabled Oyo to easily grow their business, without having to start from scratch.

They have also expanded their reach in Japan by acquiring one of its largest rental apartment operators for $100mn in 2020. They have entered the UK with the launch of their own brand Belvilla. Similarly, they have expanded in US with launch of 300 new properties and also south-east asian countries, where they are focusing on luxury hotels.

What we are trying to get to is, Oyo’s ambitions are quite big and not limited to India. This brings in lots of revenue growth and expansion opportunities, but also carries risk. We will understand later how Oyo had to scale down its international operations as they faced heavy losses. Market risks and forex risks were mounting on their head, its Chinese subsidiary had defaulted on major payments to Oyo India, and its US and South American subsidiaries were burning cash. However, now Oyo seems to be back on track and has recovered, as international businesses seem to be doing quite well.

Why do small hotels/ homestays like to partner with OYO?

In a digitised world, in order to compete with the big players, every hotelier needs to have a standard level of service and ability to market. For standalone players, it becomes difficult which is where OYO steps in. It solves pain points like:

Lack of distribution & online presence

Limited marketing

No brand loyalty

Cumbersome back-end processes

Tying up with OYO can help hotel owners increase their revenues by ~1.7-2x which means their earnings are better even after making payments to OYO.

On average, OYO takes home 33%-37% of the total gross booking. The bookings are made through the app, website, and a large network of travel agents and corporate clients.

As of last year (March 2023), OYO had a network of 5,300 travel agents across the country, which has increased this year to over 10,000. In the same year, during the first half, OYO recorded a 20% increase in corporate accounts, which makes up a significant portion of their revenue. They currently have roughly 15,000 small and medium corporate accounts, providing them with recurring business.

OYO has been doing reasonably well in India but not as well overseas. They had to reduce the number of countries they serve from 80 to 35 to focus on profitable locations and eliminate cash-burning operations. Despite this, overseas revenue increased by 12% in 2023.

The cost structure of the company can be divided into items above and below the contribution margin line. (Revenue - Variable Costs)

Take rates from hotels, transformation budgets given to owners to revamp their property, minimum guaranteed revenue given to hotels, and discounts on booking, all of these expenses are adjusted from revenue to reach contribution margins.

If we look at the financials of OYO, their contribution margins increased from a meagre 13% in FY19 to 41% in FY23. In its recent FY24 annual report, contribution margins have jumped to a record high of 45%.

This is a significant achievement, which is driven by higher take rates (around 33-37%), lower discounts, the removal of minimum guaranteed revenue to hotels, and most importantly, lower one-time costs such as transformation budgets.

These efforts are also seen in the EBITDA margins which increased from -55% in 2022 to 13% in 2024.

As per the annual report of 2024, the numbers have improved even further. For the first time, OYO has reported a net profit and a positive EBITDA margin. And yes, the numbers are without any adjustment.

(Source - Annual Report)

The improved numbers were mostly on the back of reduced fixed costs. Employee benefit expenses reduced from 28% of revenue to only 14% of revenue. This was on the back of layoffs and Oyo shifting a lot of its international operations to India. Currently 70% of the entire global workforce operates from India.

Another important line item - the marketing and advertising expenses came down from 8% of revenue in 2020 to meagre 1% in 2024.

Finance costs however have started to increase and are currently 16% of the revenue, they may create a drag on the book, but it seems that Oyo has done something about their debt situation (which we will see later). Commissions and brokerage have increased slowly, which shows that the agent network of Oyo may be one of the reasons behind revenue growth.

Before jumping to the future outlooks, let's quickly touch upon an important point. We saw the fixed costs of the company decreasing quite rapidly (Employee Benefits and IT). This generally happens because the company is achieving economies of scale.

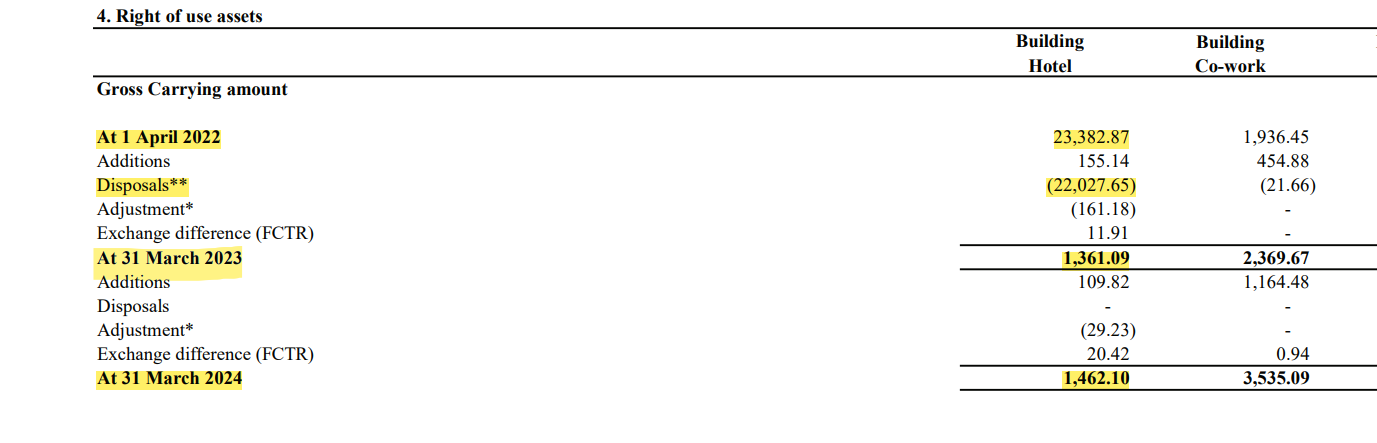

Another interesting detail we saw in the 2024 consolidated balance sheet of OYO was the ‘Right of Use Assets’ figures (Leased Properties). Oyo has hugely cut down its balance sheet by not renewing various hotel leases and shifting to a majorly franchisee based model.

With more than 18,000 properties, Oyo only has ₹146cr of lease and ₹300cr of ‘Property, Plant and Machinery’ on its books. This highlights that future expansion will be tech-led and Oyo will not need huge capital to fund it. The excess revenue generated by future expansion will hugely improve profitability thanks to economies of scale.

This also protects Oyo in any adverse macro-economic condition, as the fixed costs will be much lower and lease/fixed assets will not be on their books.

Now coming to future outlook - OYO is almost a perfect turnaround story. Back in 2020, the company faced losses of nearly 100%! They had too many overseas subsidiaries, most of them losing money, and some even defaulting on debt payments to the parent company in India.

In typical start-up fashion, OYO was offering high discounts to attract customers while providing minimum revenue guarantees and renovation budgets to onboard hotels.

But today, the company has turned around its operations by cutting costs, focusing on profitability, and consolidating its vast business operations. This operational turnaround was also supported by a favourable macro environment, where tourism picked up pace and Indian domestic tourists supported the hotel ecosystem. So, what's next for the company, you may ask?

The revenue outlook seems positive, even though the topline was flat on a year-on-year basis in FY24. Macro tailwinds and a well-planned international expansion strategy will help them grow revenue. Major rating agencies expect at least 17-19% topline growth, while Oyo is expecting a GMV growth of atleast 40% as per their FY24 annual report.

OYO is focusing more on branded hotel inventory under their various collections to improve the experience and expand profitably.

For Europe expansion, acquisitions still seem to be the trick, however there doesn't seem to be any M&A on cards for FY25. Oyo is going big on its homestay businesses in Europe, Japan, UK, and US.

South-east Asia expansion is driven by organic growth and tech-cum-hospitality approach. Oyo is majorly targeting the luxury segment in this region.

A major source of bookings appears to be from corporate accounts, including sporting bodies, MSMEs, and businesses. Their large network of agents are also able to tap into the tourism boom, which will help topline growth.

Cutting costs in marketing and staff, along with higher take rates, have improved profitability over the past two years. EBITDA margins are expected to reach 15-17% by the end of FY25, but the company has already outperformed expectations by reporting a 13% EBITDA in FY24.

The company plans to control costs across its overseas business by focusing on key locations such as the Nordic countries, Southeast Asia, and parts of the UK and US, where regulations are relaxed and competition is low.

As per FY24 annual report, Oyo prepaid ₹1500Cr (30%) of its term loan in cash. It is also planning to refinance the remaining term loan of approximately ₹3500Cr at lower interest rate, which will reduce their finance cost from 14% to 10%, saving around ₹130Cr in expenses each year.

Given the strong macro factors along with stable revenues, improving margins and better debt coverage position, Fitch recently upgraded Oyo’s rating from ‘B-’ to ‘B’.

Overall the company seems to have come out of the turbulent times, with revenue outlooks looking positive, and margins improving. The debt coverage position and cash-in-hand has also improved.

Lastly the valuations, even the best of businesses may not look investible at wrong valuations.

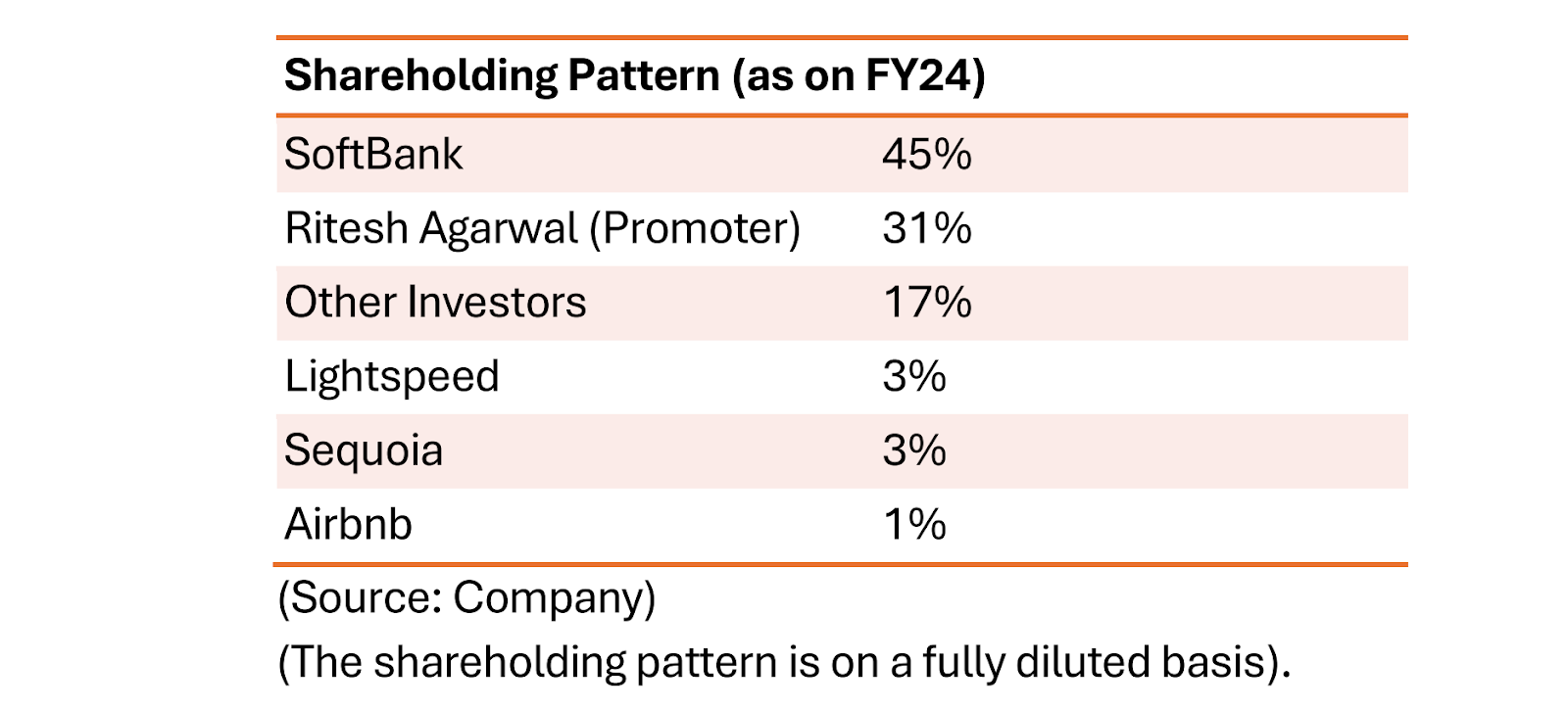

First let's look at the shareholding of OYO as per annual report of FY24 - (RA Holdings belongs to Ritesh Agarwal).

OYO's valuations were steady until June 2024, when they had to undergo a down round. The post-money valuation dropped from a high of $9.6 billion to $2.38 billion where OYO raised ~$175 USD Mn.

Valuing a startup like OYO is challenging. Discounting cash flows doesn't work because near-term growth will be high, and terminal growth is uncertain. Using multiples like EV/EBITDA or P/E ratio also doesn't make sense due to the low profit but high growth trajectory.

If we compare OYO to companies like EIH, IHCL, Yatra, and Zomato based on Market Cap to EBITDA or Market Cap to Sales, it would make more sense.

Yatra's Market Cap to Sales is 4.5. By that measure, OYO's market cap should be ₹26,000 crore or roughly $3.2 billion. However, this valuation doesn't account for the high growth of OYO's business.

If we look at IHCL (Taj), whose earnings growth may reflect the hotel sector's growth rate, its Market Cap/EBITDA multiple is 39. If we assume an 18% EBITDA for OYO in the long run, based on today's revenue, the market cap would be ₹40,000 crore or $5 billion. However, IHCL's market cap includes the book value and fixed assets of the company, which OYO does not have.

To give you a comparison, Zomato also had a comparable turnaround story, it moved from loss to profit but investors were questioning its valuation as well when it was going for an IPO. It will also be difficult to value companies like Zomato, OYO which are monopolistic/ duopolistic in nature and have a rapid growth rate.

Therefore, the fair market cap range should be somewhere between these two extremes. However, we cannot make a definitive comment on this because valuation methods vary according to analysts' views of the sector and the company.

OYO’s valuations and fundraising, as we discussed earlier, have been nothing less than a roller coaster ride. Their valuation peaked at $10Bn in 2019, and ever since, it has slowly slipped downhill. Along with numerous fundraising rounds, OYO also filed for IPO in Indian markets on 2 occasions between 2021 and 2024, but both times the company recalled their DRHP.

In its most recent funding round, which is also called the Series G Round, they raised roughly ₹1450Cr at a valuation of ₹19,700Cr (~$2.4bn). While OYO’s latest deal has happened at a steep discount to its previous funding round, there is one very positive sign - Promoter Buying.

Ritesh Agarwal has consistently participated in funding rounds, buying shares through his Cayman-based entity. In 2019, he took a massive loan of $2 billion from Japanese banks to buy a 20% stake in his company and also provided old investors with their much-awaited exit. In fact, in Series G, Ritesh bought another $100 million worth of stake through his Singapore-based entity.

Ritesh himself owns roughly 6% of the shares, and his Cayman entity owns around 23%. After this round, his Singapore entity has acquired roughly a 4% stake. Promoter buying like this builds confidence in a company, as no one knows the internal situation of a business better than its owner.

As of today, OYO seems to have shelved its IPO plans and is satisfied with the private funding route it has taken. The private round received good participation from players such as Ashish Kacholia, Mankind Pharma, and ASK Wealth Management. Thus, there is a good chance that the general public may not be able to capitalize on the turnaround story of OYO, as the IPO plans may have been delayed for another few years.

We covered the Indian tourism sector in-depth, highlighting some interesting trends. If you believe in the growth of tourism and are noticing the surge in post-COVID tourism, you can be part of it too.

Domestic tourists are boosting the industry, and foreign tourism is expected to rise as western economies recover and stabilize. Private players have noticed this trend and are increasing their capital expenditures. However, some investors may feel there aren't many good investment options in the sector or are looking for more opportunities in such saturated markets.

In that case, the unlisted markets offer unique opportunities, OYO can be a good candidate but generally be aware of how unlisted shares work, for that you can checkout the first article in our ALTShares series. For this article, we have tried to provide detailed research on the entire sector and OYO which we believe may benefit from this boom. However, personal research is essential before investing in such stocks.

Stay tuned for our next article in the ALTShares series powered by InCred Money where we will be talking about the IPL and sports industry linking them to the opportunity of investing in CSK Unlisted shares. Meanwhile do checkout other unlisted share opportunities on InCred Money.

Investment in Pre IPO | Unlisted Shares is subject to risk. This communication/ report / note / one-pager is general and educational in nature. Alpha Fintech Pvt. Ltd under the brand name ‘InCred Money’ and its representatives are not SEBI-registered research analysts or advisors. Any research, analysis, or information presented on this platform does not constitute investment advice or a recommendation by InCred Money or its affiliates. Visit incredmoney.com for the full disclaimer.

This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities.

Neither ALT Investor or its associates/associated entities, assigns or affiliates takes or accepts any liability for consequences of any actions taken based on the information provided.