The Global Race to Become Solar Leaders -The Waaree Energies Story

KEY TAKEAWAYS

The article dives deep into the competitive solar energy landscape in India, highlighting major companies like Adani, JSW, and Tata, and the growing capacity of Indian solar panel manufacturers aiming to become global exporters.

It explains the science and supply chain of solar panels, emphasizing the dominance of monocrystalline panels due to their efficiency and the significant cost contribution of PV modules.

China's dominance in the global solar market is also a big concern, with control over 80% of the market.

The details the Indian solar market's growth, which is driven by government initiatives like the PLI scheme and import duties is also talked upon, besides the ambitious expansion plans of Indian companies like Waaree Energies.

The article concludes by discussing the risks in the solar sector, particularly Chinese dumping, and emphasizes the importance of identifying companies with strong reinvestment strategies and high returns on capital employed.

There's an exciting solar race happening in India, both on rooftops and in solar parks. Big companies like Adani, JSW, and Tata are all competing to install panels and capture as much sunlight as they can.

But there's another side to the story. In the manufacturing units, Indian solar panel makers are boosting their capacity, not just to meet local demand, but also to become global exporters.

The solar manufacturing industry in India is still in its early stages and not well-known to retail investors. However, with the developments we're seeing, it's set to create some of the next big companies in India.

The next big opportunity might just be in the nearby unlisted markets, with companies like Vikram Solar and Waaree Energies leading India's solar manufacturing efforts.

In this article, we will explore every aspect of solar module manufacturing. We'll look at how the industry operates, where the biggest opportunities lie, and what the main threats are.

The Science Behind Solar Panels

To understand solar manufacturing, we need to start with the science behind it. Below is the general product life cycle of a solar panel, starting from polysilicon (raw material) to the final module.

There are a few other materials used in solar panels, but these are generally considered secondary to the main supply chain as they are part of the installation process. For example, in India, Borosil Renewable has a monopoly on solar glass manufacturing, so it benefits from any increase in panel consumption.

In the supply chain of solar panels, the PV module makes up 50-60% of the cost. The rest is the installation part, which includes glass, aluminium frame, backsheet, EVA etc.

Regarding the panels themselves, there are several types available in the market. However, as installations have increased, monocrystalline panels have become the most popular due to their superior efficiency.

(Source - International Energy Agency)

If we look at the solar supply chain, it's not necessary for all components to come from the same country or company, as production lines are often not integrated. Some companies may lead in solar cell production, while others might outsource all components and still excel in panel development.

To grasp this, we need to understand all the forces at play in the solar market.

Manufacturing Capacity & Capability

A decade ago, around 2011, the US and Europe used to compete with China in the solar market. Today, China is the largest player in every component and solar module by a significant margin, controlling over 80% of the global market. This dominance is due to the $50 billion capital expenditure announced by the Chinese government back in 2011.

Currently, China has the highest supply of solar modules but not as high domestic demand. Therefore, it is a major exporter on a global scale. The graph below may concern some, given the extent of the market dominated by China.

Even when it comes to major raw materials used for producing solar PV modules, China is the most resource-rich nation.

Currently, the top 10 companies that manufacture solar modules are all from China. This dominance in a sector that represents the future of energy worries many countries, leading to the China +1 policy, where Indian manufacturers are preferred by many suppliers to reduce overdependence on one country. This policy, along with India's own demand, sets the stage for Indian manufacturers to benefit from the solar boom.

The Indian Solar Story

To understand the Indian solar market, we need to split it into consumption and supply. In 2023 alone, India's solar manufacturing capacity saw a 2x jump, and the additional capacity was mostly to cater to domestic demand.

Thus, understanding the sudden rise in consumption is key to understanding India's solar growth story.

Consumption

As of 2024, India's total power capacity is 446GW, which is divided almost equally, between thermal projects and renewable sources - leaning a bit towards the former.

(Source - Power Ministry June Update)

The government, through its National Electricity Plan (NEP), plans to double this capacity to 900GW by 2032. What's so impressive about this?

The majority of this capacity increase will come from renewable sources. In the next 5-6 years, 50GW of renewable capacity will be added each year, boosting renewable capacity from 200GW to 500GW by 2030. Out of this 500GW, 250GW or 50% will come from solar installations, while the rest will be from hydro, wind, and nuclear sources.

You can now see why solar is a hot topic in today's market. The government is planning a massive expansion in India's energy capacity, led by solar installations.

This expansion aims to reduce peak energy deficits and meet the growing energy demand. The biggest beneficiaries of this initiative will be Indian solar module manufacturers, who are ready to invest heavily in capital expenditures. It seems their time has finally arrived.

Supply

In the past 4 years (2020-2024), India's solar installations have increased by 15-18GW each year. In 2022, our solar module capacity was just enough to meet domestic demand. However, some of this capacity was export-driven, and others were likely not operating at full capacity. As a result, we still had to import almost 50% of our domestic demand from China.

(Source - Waaree Energies DRHP)

In 2023 however, our module capacity jumped more than 2x, which hugely helped in catering our domestic demand, while also increasing exports by more than 10 times!

(Source - IEEFA)

But simply increasing module production capacity will not help, as we will still have to import our raw materials from China. If you look at the above chart, we have the capacity to manufacture 38GW worth of solar panels, but only 6GW of solar cells, and almost no capacity for ingots, wafers, and polysilicon! This means we will still be dependent on China for all the components used in solar modules.

The Indian government and industry players have realized this and have started building fully integrated capacities to produce all components in-house.

Indian Market - Players

Let's introduce our Indian solar manufacturers and their market share as of today.

(Full list - Here) (1000MW = 1GW)

As of the latest available data, Waaree Energies leads the Indian solar market by a significant margin. However, Adani might get much closer to the top spot after the next round of capacity expansion.

All the players in the list above have announced their expansion plans. In the list below, we can see that most of the players have also announced their plans for solar cells. Many of these players are building integrated facilities in the next round of expansion, which will include at least one or more components of the solar module.

(Source - Waaree Energies DRHP, CRISIL Consulting)

If you look closely at the list above, you'll notice many new entrants with significant capacity addition plans. Reliance, Shirdi Sai, Tata Power, and Jupiter Power, who were absent from the first list (of installed capacity), are now showing big numbers in the next round.

Why is this happening? It's all thanks to government initiatives promoting solar module manufacturing in India.

Government Initiatives

There are two major initiatives that are taken by government to protect and promote the above seen businesses.

PLI Scheme

Production-linked-incentive scheme incentivizes companies for any additional goods/services produced in India compared to the base year. The incentives can be in the form of tax rebates, concessions on import/export duties, etc.

The government has decided on an outlay of ₹24,000 Cr for high-efficiency solar modules. This means all sales generated from the capacity set up under the PLI scheme will be subject to incentives based on solar module’s temperature coefficients (used to measure longevity and efficiency) and Local value addition factor (sourcing of raw material).

Thus, companies like Reliance, Tata, and JSW, who were not seen in this race earlier, are now dipping their feet in the hot water.

(PLI Tranche 2 Full List - Here and Here) (1000MW = 1GW)

The table above shows which companies received capacity allocations under the PLI scheme. The bidding was done in brackets based on how integrated the facility is. For example, Indosol and Reliance won bids for fully integrated (all 4 module components) capacity, while JSW and Waaree won bids for partially integrated capacity, which includes only 3 components, excluding polysilicon.

Tariff And Duty Structure

Chinese dumping is a practice where China sells goods in a foreign country at a price lower than their domestic selling price, after accounting for transportation expenses, tariffs, and other costs. This practice is gradually impacting India's progress in the solar industry because consumers are buying cheap Chinese solar products instead of Indian-made ones.

To support Indian solar manufacturers against Chinese imports, the government decided in 2022 to impose 40% import duties on solar modules and 25% duties on solar cells. Several anti-dumping duties were also placed on Chinese imports to prevent an oversupply of modules in the country.

This covers most aspects of the solar industry in India. For those interested in this sector and considering investing in some of the key players, let's take a look at one of the top solar manufacturer in India available in the unlisted markets.

Waaree Energies

Waaree is the biggest Indian player in terms of capacity, with about 12GW of Module production capability per year. That's roughly, 1/3rd of India's overall capacity!

Waaree Energy is also a darling of promoters amongst their massive Waaree group empire. There are 2 other listed companies of the group are also in the energy space:

Waaree Technologies is into battery manufacturing.

Waaree Renewable Technologies is into large scale EPC contracts for solar, hydrogen, etc.

Before diving into future expansion plans, which are quite ambitious, let's start with a brief overview of the company and its finances.

Ownership and Shareholding

Currently the promoter group - Doshi Family, owns upwards of 70% of the company. In June 2023, the company raised ₹1,000Cr funding from various Investors to fund its new integrated 6GW plant. As of today, the structure remains the same.

Business Model

Now, let's look at the financials. The company increased its revenue by 50% in FY22 and then doubled it in FY23 and FY24. Waaree is primarily an export-driven business, with about 70% of its revenue in FY23 coming from countries like the US, Canada, Hong Kong, and Turkey. However, this shifted in FY24, with 40% of the revenue coming from domestic operations. This change is expected, as the growing demand for solar energy in India is a major driver for revenue growth among local players.

Waaree's business model is straightforward. The company imports most of its raw materials and components from countries like China and uses them to manufacture the final product, which is solar panels.

These panels are then sold through 3 channels.

Direct sales to utilities and enterprises generate the majority of income in India (70% of domestic sales).

For export-driven sales, Waaree has a customer base in the US, Canada, Hong Kong, Turkey, and other countries (60% of overall revenue).

The rest of the income comes from franchise and distributor sales in India, also known as retail channel sales, which make up 30% of domestic sales.

A very small part of the revenue (~1%) comes from EPC contracts for solar parks and site installations.

Financials

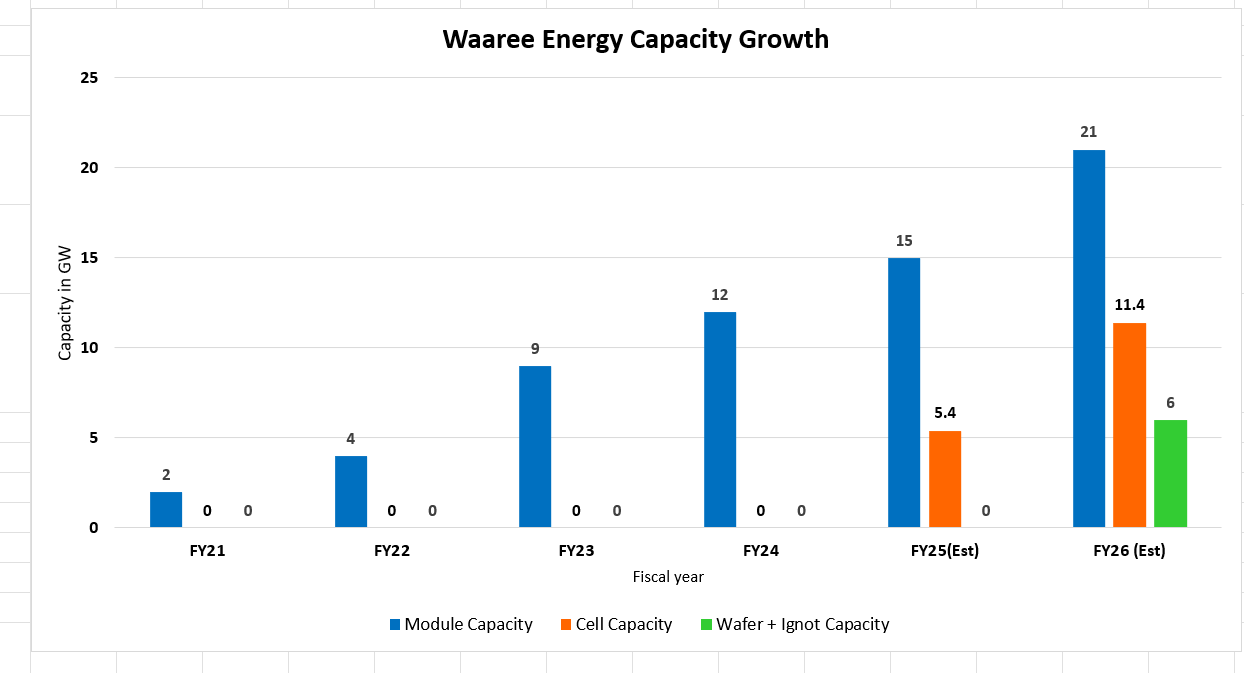

Before looking at the financials, let's look at the module capacity growth of Waaree Energies. Without this, the revenue growth will leave your head spinning. From 2020 to 2023, the company has increased its manufacturing capacity by a whopping 6x! And the capacity expansion doesn't seem to be slowing down in the coming years.

Now let's look at the topline. We can see the huge jump in the revenue in FY23 and FY24, this is thanks to the unlocking of module capacity from 4GW in 2022 to 9GW 2023, and further increasing it to 12GW in 2024.

Similarly, if we look at the some of the important ratios for a manufacturing company (ROCEs, EBITDA Margins and D/E ratio)

As the company is currently in the capital expenditure (CAPEX) phase, the Return on Capital Employed (ROCE) will be under pressure, and margins may not accurately reflect the true state of the business. Nevertheless, ROCE is improving, EBITDA margins are becoming more favorable, and the Debt to Equity (D/E) ratio remains negligible, as growth is funded entirely by equity.

If we look at the balance sheet of Waaree Energies, we can see that the company did a CAPEX of ₹1000Cr last year (Dedicated to Solar Cell Facility), and has increased it to over ₹1200 Cr this year. The cumulative capital-work-in-progress of the company is 1.3x its current plant and machinery value! This is a massive capacity expansion we are seeing in the sector.

If we again take a close look at the balance sheet, we can see that the company has roughly ₹3700Cr cash in hand, thus should have no notable difficulties in financing future projects.

(FY24 and FY23 respectively)

Another key thing to notice is the ‘other current liabilities’ ballooning up. These consist purely of contract liabilities, which shows that orders are piling up. Thus, increase in capacity will be felicitated by already surplus demand.

Even if we look at the below table, the order book of Waaree is 2x its annual capacity.

Source: Waaree Energies Annual Report FY23-24

Growth Prospects

The growth prospects of Waaree Energies is quite clear. Expand the solar module capacity and focus on building integrated facilities i.e. including Solar Cell, Ingots/Wafer and Polysilicon manufacturing capabilities.

We can also see that Waaree is planning not only major domestic expansion, but also expansion in the US. This is obviously to cater to its North American Clientele.

In domestic expansion, the solar capacity will increase from 12GW to 19GW, while the solar cell capacity will increase from 0GW to 11.4GW. These are massive projects that will help Waaree keep its market leader title, while becoming a major player on a global level.

Risk Prevalant In The Solar Sector

So, the domestic macro factors are great. The government is supporting local manufacturers through PLI schemes and import duties, while also boosting solar demand by setting ambitious targets for PSU, state, and private utility players.

Should we, as retail investors, blindly invest in anything related to solar manufacturing? After all, it's the next big thing. The answer is NO, at least not without proper research.

There is one problem troubling the solar industry in India: Chinese dumping. Let's summarise this issue quickly.

China has a huge over capacity for Solar module manufacturing (We already saw that). Now that the demand in China has stagnated and is reducing, Chinese manufacturers are finding it difficult to sell their panels. So they naturally offload it in the export market, thus driving the global prices to rock bottom.

The below graph shows how prices of solar cells and wafers have reduced by 75% in the last 2 years.

Even the price of polysilicon has plummeted in a similar fashion.

The above plateau like shape is very common in other goods as well, such as fertilisers, chemicals, consumer durable OEMs etc. During Covid-19, due to major supply chain disruption in China, the prices of such goods soared.

But post the housing bubble burst and weak Chinese economy, the country faced a situation of over-supply and weak demand. And the spillover effect of this situation was faced by global manufacturers, as Chinese players dumped excess inventory in global markets.

Such is the power of over-capacity of Chinese players.

This situation had affected Indian players in the domestic market, as imports from China had surged by 70% in April 2023. However Indian players found shelter in export markets, where US and Allies had stopped imports from China.

But this situation increases the uncertainty in the solar business, raising the risk of investment. The main risk for solar companies still comes from China. Since most components for solar panels come from China, any issues in trade relations with the country could disrupt the solar industry in India.

Conclusion

One thing is very clear: the solar race is just getting started. With support from macro factors and government incentives, many players will compete to add capacity and become leaders in this space.

Risks such as Chinese dumping will exist and may occasionally disrupt progress, but given the demand for solar modules, the industry will grow in the long run.

It's up to you to identify which player will benefit the most on the supply side. A good rule of thumb is to look for companies that are reinvesting the most cash flows and earning better returns on capital employed (ROCE).

Often, the annual capital expenditure of larger players like Waaree is equal to the entire fixed assets of smaller players. If companies like Adani and Waaree can maintain higher ROCEs, thanks to integrated facilities and economies of scale, their stocks can become consistent compounders. So, if you spot opportunities like these, consider them for your diversified portfolio.

If you are fascinated by the solar industry and want to explore Waaree Energies or Vikram Solar, you can check out InCred Money. If you are not aware of how unlisted shares work, you can check out our first article in the ALTShares series here. In this article, we have tried to provide detailed research on how the Solar industry works and Waaree Energies as an investment option. However, personal research is absolutely essential before investing in such stocks.

With this article, it brings us to an end of the ALTShares series atleast in the form of Season 1. We hope you enjoyed the series and found our research objective and interesting. We hope to see you soon for Season 2!

Investment in Pre IPO | Unlisted Shares are subject to risk. This communication/ report / note / one-pager is general and educational in nature. Alpha Fintech Pvt. Ltd under the brand name ‘InCred Money’ and its representatives are not SEBI-registered research analysts or advisors. Any research, analysis, or information presented on this platform does not constitute investment advice or a recommendation by InCred Money or its affiliates.

The information mentioned on the platform is based on publicly available data and to the best of our knowledge, does not constitute insider information. Visit here for the full disclaimer.