Understanding Compulsory Convertible Debentures (CCDs) From A Retail Investor's Perspective

Investigating the Realm of CCD Investments in India

I am a CFA and FRM Charterholder. I used to work as a Portfolio Implementation Manager for Aviva Investors managing £3bn+in Assets Under Management in the UK. I am very passionate about educating people on how they can make more money with their existing investments sustainably.

KEY TAKEAWAYS

Compulsory Convertible Debentures (CCDs) are popular in startup investments, offering a way to raise capital when valuations are uncertain, and they convert into equity within 10 years.

CCDs are considered equity instruments by the RBI but do not appear on a startup's cap table until conversion, and they typically offer lower interest rates compared to Non-Convertible Debentures (NCDs).

A sample CCD contract from TykeInvest highlights key terms, including interest rates, conversion conditions, and liquidation priorities, emphasizing the importance of understanding exit options.

CCDs do not provide voting rights until conversion, and investors face risks if the issuer defaults, but they are safer than CSOPs due to RBI regulations and liquidation payment priority.

Currently, no platforms facilitate retail investments in CCDs due to advertising restrictions, and secondary sales require company board approval, making thorough examination of agreements crucial.

CCDs, as instruments, are not new to the startup investment community; in fact, they are often the preferred method for raising capital for early-stage startups. However, CCDs gained significantly more popularity when fundraising platforms like Tyke enabled retail investors to participate in such deals. Although most platforms now have stopped allowing retail participation in CCDs due to Tyke's close escape with the Registrar of Companies, it is still beneficial to know more about this structure in case it becomes popular again.

1. CCD (Compulsory Convertible Debenture)

In simple terms, the Compulsory Convertible Debenture (CCD) is an effective financial instrument for raising capital when startups and investors are uncertain about their valuation at a very early stage. It is essentially an unsecured loan that pays interest and must be converted into an equity stake in the company within 10 years. (this is as per RBI rules under Companies (Acceptance of Deposits Rules, 2014)

From the Reserve Bank of India's (RBI) perspective, a CCD is an equity instrument. However, it does not appear on the startup's cap table until it is converted into equity. But depending on your CCD agreement, the company will have to pay you a certain interest rate until the CCD gets converted.

Since compulsory convertible debentures are required to be converted into equity, they typically pay lower interest compared to Non-Convertible Debentures (NCDs), which are a pure form of unsecured loan without any collateral.

Also just to advise, any gains on CCDs are considered Capital Gains and are taxed accordingly. NRIs can also invest in CCD via the FPI route but this is not very straightforward and a normal retail investor will not be able to deal with compliances so we will not go into detail here.

2. Let's take a look at a sample CCD contract

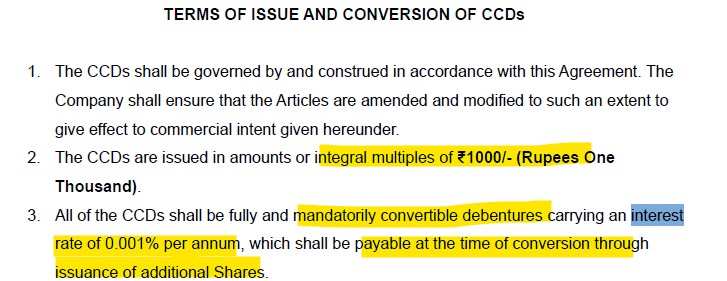

The below contract is a sample contract issued by TykeInvest and made publicly available on its website a few months back but since has been removed as they have stopped dealing in CCDs. You can download the contract from here. I am only mentioning the parts important from this article's perspective.

What do you get with your investment?

You get CCDs issued in multiple of 1000 rupees which would pay 0.001% interest per annum, so in effect 1 rupee every year, which ultimately would get converted into equity by the issuance of additional shares. Unless your investment is huge, this wouldn't generally make a huge difference to you.

Please note, other CCD deals might have higher interest than this, this is just a sample agreement.

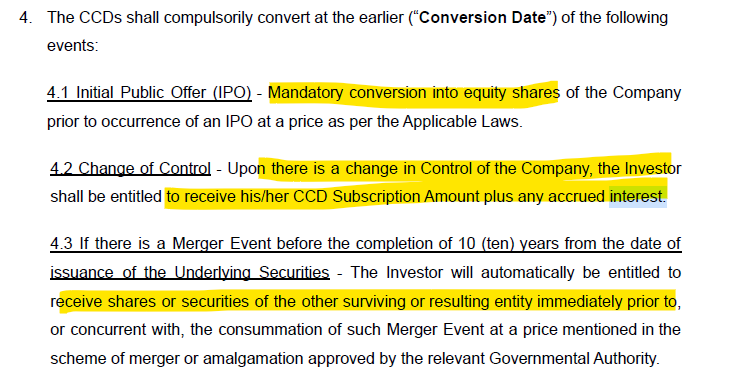

When do CCDs convert to Equity?

All of the above is pretty standard except Option 4.2 where it is not clear if the investor receives just his investments back or receives the fair value of equity at the time.

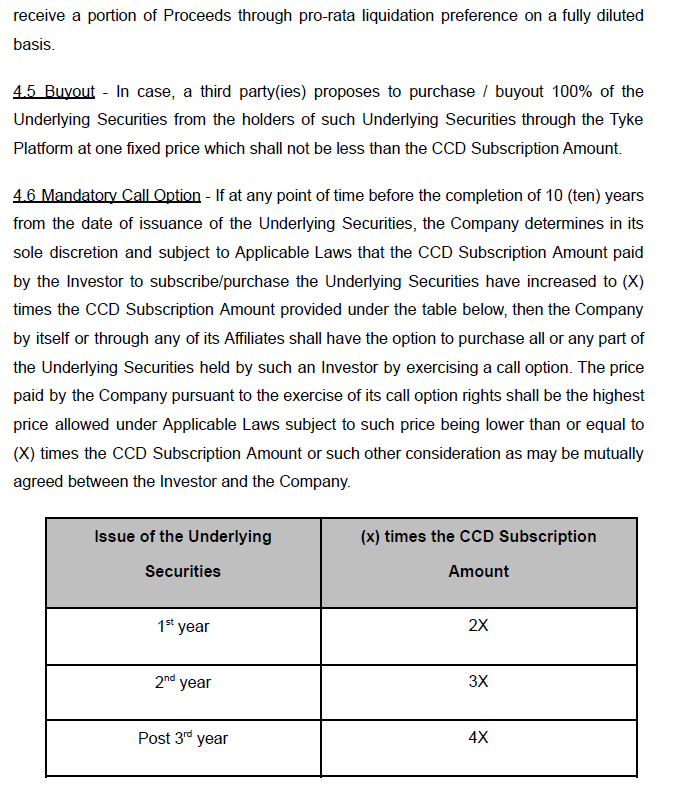

Investors should also be mindful of Option 4.6, where the company can call back your CCDs at a defined multiple of what you invested.

E.g. If you invested 50,000 INR in PhonePe CCDs in 2018 and were allocated 50 CCDs paying 0.001% interest, and the company's valuation increased by 100 times in 2023 (5 years from the CCD issue date), the company could simply buy back your CCDs for 200,000 INR if the multiple is 4 times, completely excluding you from the upside they experienced.

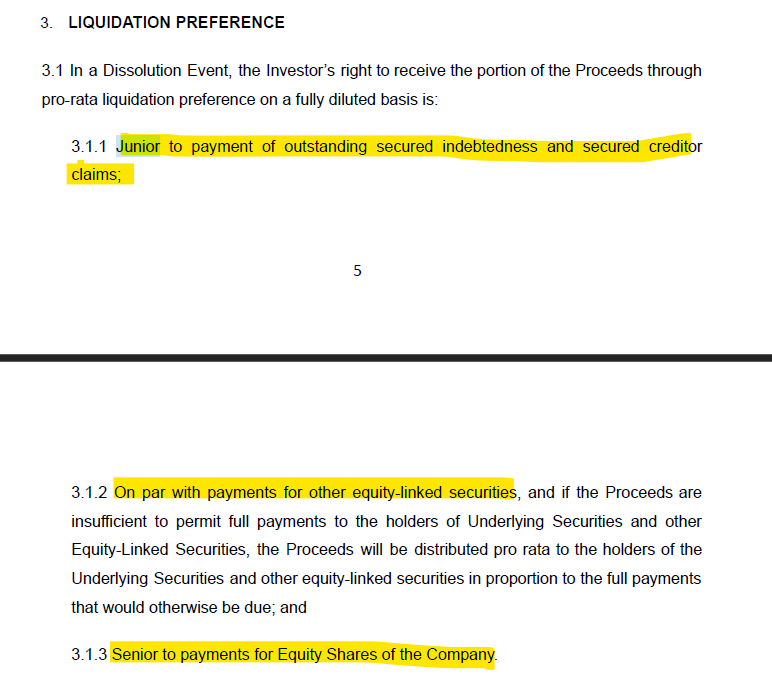

How is your investment treated if the company is liquidated?

Essentially, this means that you are second in line for your money. First, proceeds go to secured debt products; next, they go to you and other equity-linked instrument holders like CCDs; and finally, they go to promoters and equity shareholders of the company. This aspect of CCDs can be seen as positive.

3. Other Red Flags to Consider

You don't own any voting rights in the company until your CCD is converted into equity.

If the CCD issuer defaults, they might be unable to pay back your principal invested and offer you a bigger equity stake but what is this equity worth if the company is not performing well?

4. Other Green Flags to Consider

It is much safer than CSOPs which are also trending in the investing community as they have set regulations by RBI and a set timeline (max 10 years)

They are 2nd in priority for payment in case of liquidation of the company.

They get converted into equity which can value significantly higher for a few startup companies and good way to create wealth.

5. Bottom Line?

CCDs are a reliable and secure category of instruments for gaining early-stage startup exposure while ensuring a stake in the company's future. However, as demonstrated earlier, these deals can be highly customizable, so it is essential to thoroughly examine the fine print regarding all exit options in the CCD agreement.

Based on my research, at present, there are no platforms available for retail investors that facilitate investments through CCDs, as these deals cannot be openly advertised to more than 200 people. If you are aware of any such platform, please feel free to correct me in the comments below or email me at yash@thealtinvestor.in.

Please note that this is an opinion blog and not official research advice. I am not a registered RIA in India, and none of these views reflect those of my current employer. This blog aims to promote informed decision-making and does not discourage you from investing in any deals.

We plan to come up with more blogs discussing different types of instruments available in the world of startup investing, write on due diligence for some platforms, and also existing and upcoming alt investment deals in the Indian market. If you want to stay updated on the latest blogs, please subscribe to our newsletter so you get notified automatically, if you are a Tradewithpython subscriber, you know we don't spam.

Lastly, if you like our work, please feel free to sponsor us via Hashnode Sponsors or Buy me a Coffee by clicking here or the button below. And if you would like to speak to me or get my opinion on anything related to investments/finance/algotrading, schedule a call with me on Topmate.io by clicking the below image.

Thank you for reading and hope to see you in the next one!