Understanding Infrastructure Investment Trusts (InvITS)

Search for a command to run...

No comments yet. Be the first to comment.

In this series, we cover all instruments, schemes and products in the alternative investment space available for Indian retail investors.

KEY TAKEAWAYS Gold has been a traditional symbol of wealth in India, and there are multiple investment options available for those looking to invest in gold from an investment perspective. Gold is considered a good hedge against market volatility, ...

Many of you might have invested in Reliance Industries, TCS, HDFC Bank, SBI, or Infosys. After all, these are amongst the biggest companies in India which are listed on the stock market, so you can co

Real estate has traditionally been a “high-ticket” asset class. Either having lakhs (or even crores) of Rupees in your bank account or taking a huge home loan were the only two prominent ways to buy property. But that is changing now with fractional ...

India’s Finance Minister Nirmala Sitharaman is set to present the Union Budget this week on February 1st, 11 am. This will be her ninth consecutive Budget presentation, which brings her closer to former Finance Minister Morarji Desai’s record of pres...

Imagine you are an absolute equity lover. Stocks are your thrill ride, while debt funds are just a sleepy side note in your portfolio. But what if I told you there were years when those ‘boring’ debt funds left the stock market in the dust? And not j...

Can I ask you a question? Don’t worry, it's not a complex mathematical problem. Just a simple one- Whenever the stock market feels noisy and makes your portfolio bleed red, what’s the one thing you secretly wish for? I am sure it must be about having...

Infrastructure Investment Trusts (InvITs) are specialized mutual funds that pool investors' money to invest in infrastructure projects like highways, power grids, and data centers, offering diversification and consistent income streams.

InvITs were introduced in India in 2016 to bring multiple infrastructure projects under one vehicle, diversifying risk and making it easier to invest in such projects.

The structure of InvITs involves a trust set up by a sponsor, with a trustee and asset manager overseeing investments, and SEBI regulations ensure 80% of assets are cash-generating and 90% of profits are distributed to investors.

InvITs generate cash from various sources, including dividends, interest, and capital gains, with different tax implications for investors, making understanding cash flows crucial.

While InvITs offer predictable cash flows and lower risk, they require thorough research due to factors like asset type and investment manager performance, and they come with complex tax considerations.

Do you want to guess a key skill that differentiates one wealth manager from other wealth managers? No, the answer is not fundamental or macro analysis. It's 'storytelling'. Any analyst or manager can perform the basic analysis, and pick up fundamentally and technically sound stocks. But to sell the idea of an investment, the fund manager needs to sell a story. Take Saurabh Mukherjea for example, the poster boy of long-term investing in India. Every stock in his portfolio has a story behind it, connecting the company to a broader and larger picture. Thus, he is able to sell his ideas to his investors (Even with not-so-phenomenal returns).

A similar observation can be made in the InvITs (Infrastructure Investment Trusts). It is not an extraordinary piece of investment, but the government sold a sensational story to retail investors during the IPO of NHAI InvIT, to increase their participation in this investment product. The story went something like, 'Retail investors can now contribute in the nation building, infrastructure and economic growth of the country'. And this got me curious, can retail investors really put a dent in the infrastructure funding space, where institutions and governments have already poured billions of dollars? And the second question, which is actually the most important one for me, can InvITs provide a consistently decent return for a longer duration? Well to answer these questions, we will have to explore InvITs together and understand what they have to offer.

InvITs stands for Infrastructure Investment Trusts. In very simple terms, InvITs are like specialized or sectoral mutual funds. They pool investors' money to invest specifically in cash-generating or under-construction infrastructure projects. Here, Infrastructure assets refer to capital-intensive projects such as Highways, Dams, Railway projects, Power Grids, Transformers, Data Centers etc.

InvITs may also invest a small portion in money market instruments, equity instruments or other liquid securities for cash management purposes, but their bread and butter are the infrastructure assets.

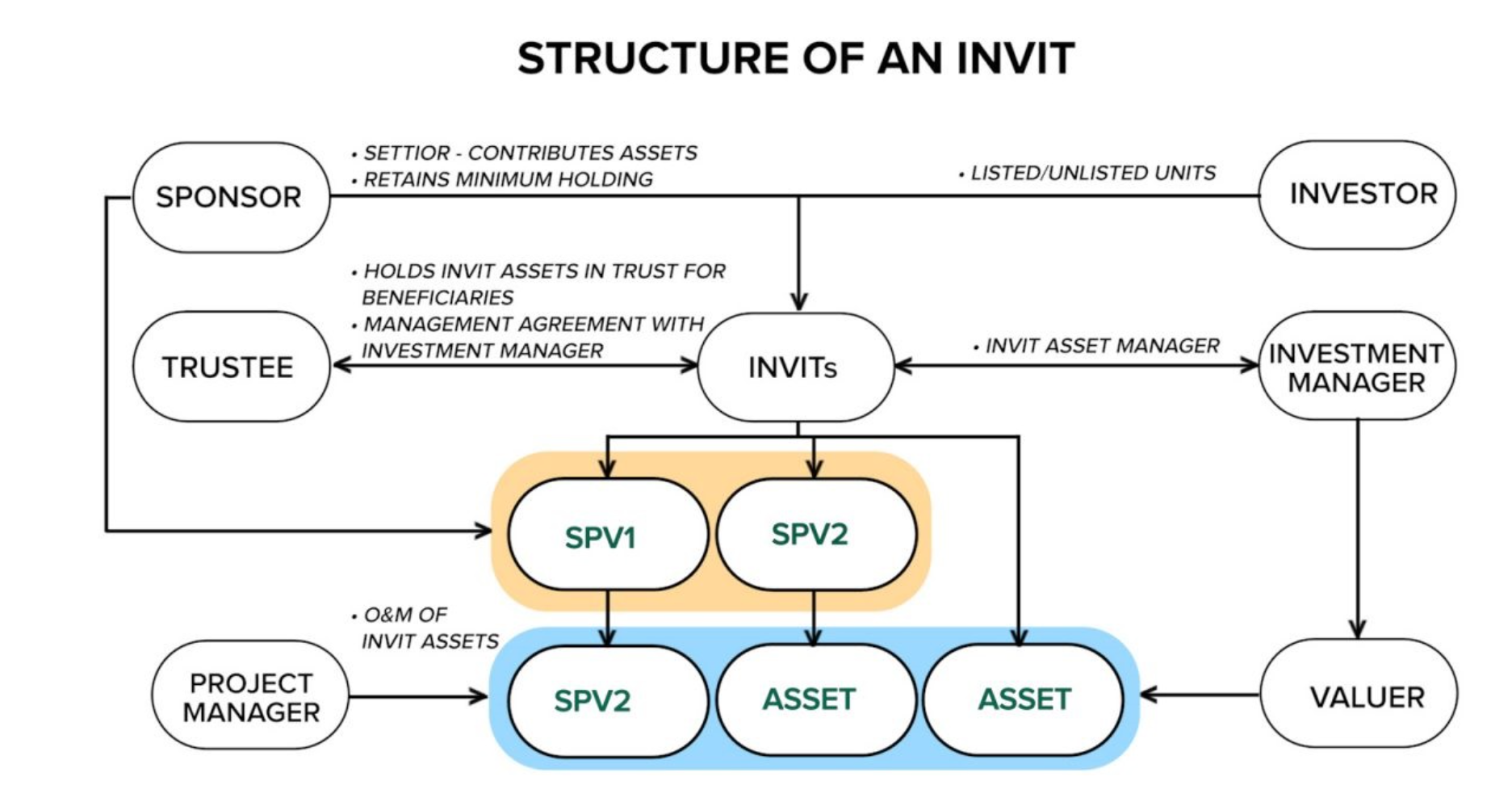

To explain this, we will have to go back to 2016 when SEBI approved the structure of InvITs and allowed them to list on stock exchanges or raise money through private placements. The structure of InvIT was introduced to bring several infrastructure projects under one common vehicle or common roof. This was done to diversify risk and make investing in such projects easier.

Still confused? Let me explain. If you see the AGM report of any infrastructure company or a Real estate developer, most of their projects are in the form of an SPV (Special Purpose Vehicle)

Take the example of Lodha (NSE: Macrotech Developers), you will see that the company has a separate SPV for different projects. So one SPV for the building in Lower Parel and another SPV for the one in Goregaon. Now, in such a situation, if the company wants to raise money for a specific project, it will have to issue shares of the SPV and not the parent company. So naturally, Investors are hesitant to fund the project. This results in a lack of capital and a high cost of long-term debt. All of these problems are solved by InvITs, builders get easy access to capital and monetize the assets, while investors get to diversify their portfolios with consistent income streams and okay-ish liquidity.

The two most important features that differentiate InvITs and make them an investible product are the structure of the scheme and cash flows inside and outside of InvITs. Let us see how.

The structure of an InvIT is more or less similar to mutual funds. The sponsor of the fund sets up a trust where the investor's money is pooled. This trust itself is called InvIT. The sponsor appoints a trustee for the trust and an asset manager/ asset management company to oversee the investments and operations of InvIT. To raise money, the InvIT will go for an IPO. The IPO is similar to that of an equity share, the price discovery is done through a book-building process and investors are allotted units in the trust.

Source: ET Money

So now the question is, what happens to the cash which is raised? The money is used to invest in various infrastructure projects through separate SPVs. This is where SEBI starts playing with the rules to ensure capital protection, minimize risks and protect investors' interests.

According to SEBI, 80% of all the assets of InvIT should be cash-generating assets. In other words, projects which are already complete. Also, SEBI has mandated that 90% of the total profits of an InvIT in a year, should be distributed to its investors. Such regulations allow investors to predict a good chunk of the future cash flows and this also makes InvIT a safer investment.

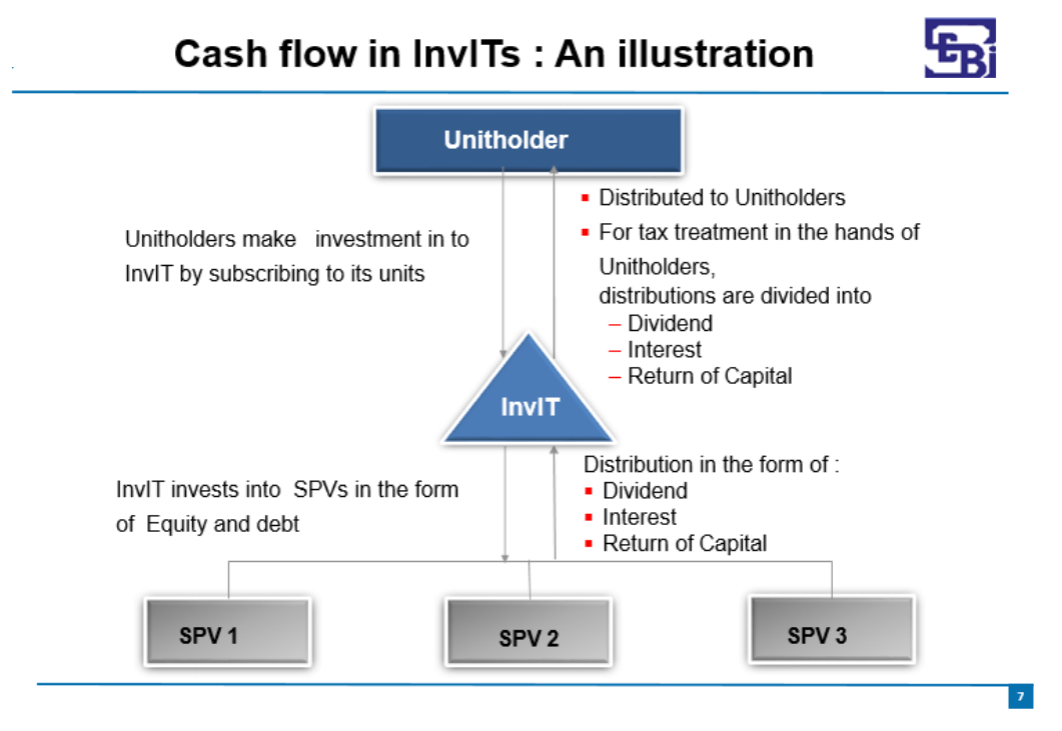

Cash Flow is one of the most important features of an InvIT as it generates cash from various sources. Also, understanding cashflows is key to understanding the taxes on these products, as investors get a few tax benefits along with several tax incidents.

Once the InvIT raises funds from investors, it infuses these funds in the SPV in the form of equity and debt. InvIT may also hold treasury instruments and certain equity instruments to maintain liquidity. So in total, an InvIT generates cash from the following sources:

Dividends from SPV

Interest Income from SPV

Repayment of principle from SPV

Capital Gains on Investment in Instruments

Dividends/ Interest from Investment in Instruments.

Income from Assets/ Projects owned directly

Now, while distributing this income, the investors will have different tax incidence on different sources of income. Let us understand this with the help of an example. Let's say you invested in a listed InvIT, where

Avg Price Per Unit = Rs 100

No Of. Unit = 1000 (Market Value = 1,00,000)

The payout for the year was Rs.7 per unit

From the POV of Investor, the payout of Rs. 7 will be split under the following headers:

Dividend Income (Tax Exempted) - This is the dividend that is distributed by the SPVs that have chosen a higher tax regime.

Dividend Income (Taxable) - This is the dividend which is distributed by the SPVs that have chosen a lower tax regime

Interest Income (Taxable) - This component represents the interest on debt received by the InvIT from SPVs. It is taxed as per the slab rate of the investor.

Repayment Of Principle (Taxed) - Repayment of principle by SPV to InvIT is taxed as per the newly added clause under section 56(2)(xii) as income from other sources. Pls, consult your CA for this, as this is not completely straightforward. The tax incidence starts only when the sum total of all the previous principal repayment payout components is greater than the face value of all the units.

Rent from SPV or Direct Projects (Taxable) - Taxed as per the tax bracket.

Short-term and long-term capital gains tax on the sale of units before or after 1 year respectively.

The above breakdown of the payout will be provided by the fund manager of the InvIT during the payout so you know which component is taxable, but as you can see it's incredibly complicated.

There are a total of 23 InvITs in India as of 15 Nov 2023 as per this list available on SEBI, while only 4-5 are currently listed on the exchange. But, we can expect a lot more InvITs to launch in the market soon, as the government wants to monetize capex-heavy infrastructure assets on its book, and DII, retail and FIIs are warming up to this investment product.

Source: Screener

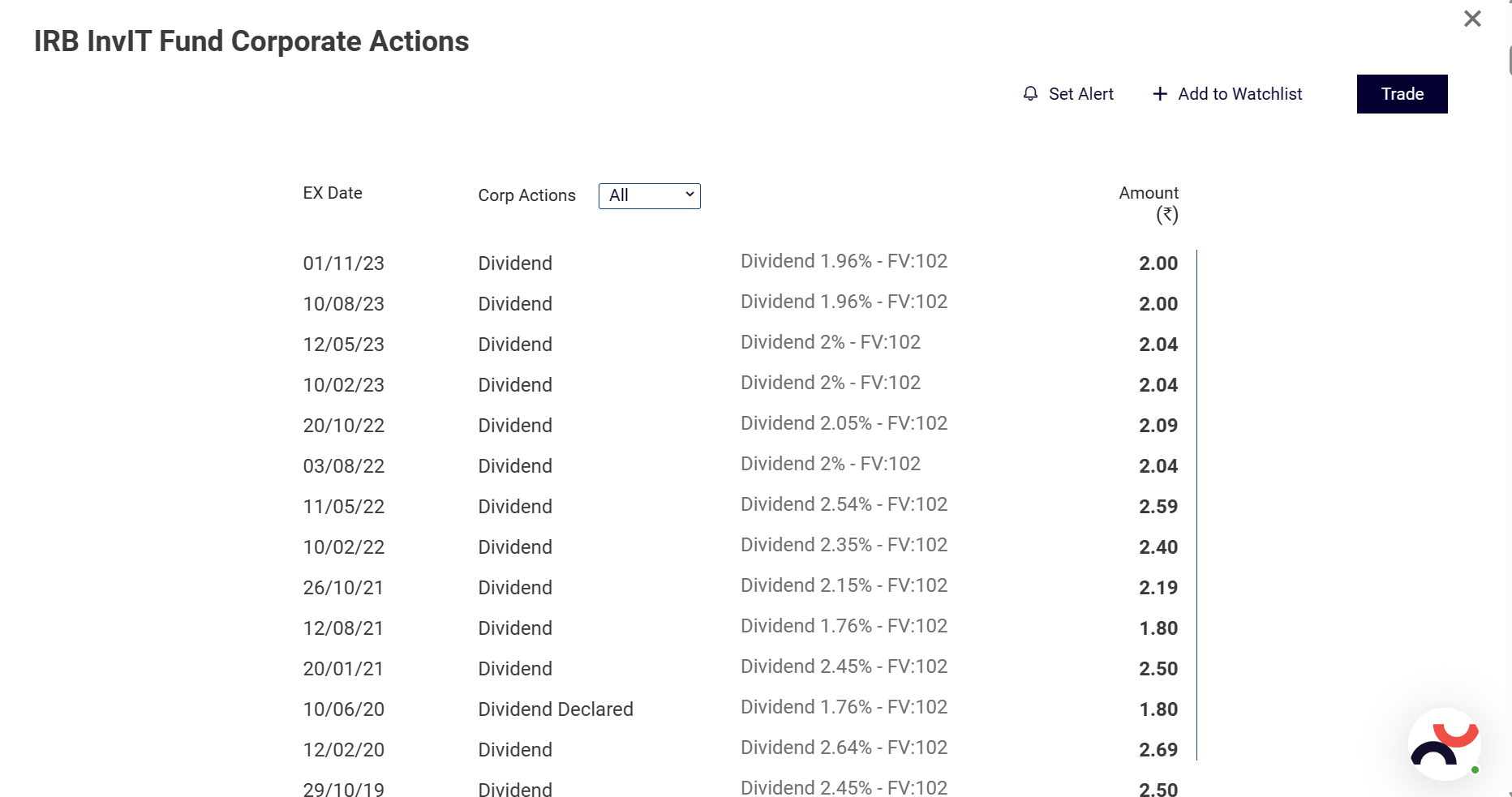

So just to analyze what returns to expect from InvITs, let's look at the historical returns of IRB Developer InvIT (dark blue line below), which was the first InvIT to be listed on the stock exchange.

In 2017, the IPO of IRB InvIT was over-subscribed to 857% or more than 8 times! The units were listed at ₹102 each, but today they are trading at roughly ₹75 a piece. This wouldn't mean that the InvITs are a bad buy, they generate good cashflows so those should be considered as well. For example, if you were to buy IRB InvIT on 2nd March 2020 when it was at its lowest for around ₹25, that would have been a solid deal as the InVIT was returning around ₹7 in cashflows yearly which would make your return on capital at 28%. Of course, nobody can time the market, but this was just to show it can be a good investment as well.

Given that there are only a handful of InvITs listed in India, there is no analyst coverage about these products. This makes this space slightly less explored, even though there is a good amount of transparency when it comes to the books of InvITs.

If we look at some of the charts of IRB InvIT, we will see a consistent drop in price even with decent payouts, what could be the reason behind this?

The reason for this price dip was because of these main reasons:

Lower toll collection from two major highway projects. The IRB InvIT saw a decline in collection from their Dahisar-Surat and Jaipur-Deoli highways, while only a marginal increase in Pathankot-Amritsar Highway.

Also, the type of projects that IRB has on their books is under the BOOT (Build-Operate-Transfer) model, which means that after a point the assets will be transferred to the government. This means that this InvIT not only has to generate a return on capital but also pay back the capital before the time runs out.

Another key reason is the type of assets, ie highways. The revenue from highways depends on various factors, such as industrial and tourist activity in the area etc. In IRB's case, there was a mining ban by the government in the Jaipur-Deoli region, which contributed to the dip in the toll collection.

Along the lines of the above point, if we compare IRB InvIT to IndiaGrid InvIT, which undertakes assets such as grid transformers, the volatility in highways is way more than that in transformers. This is visible in the cmp, IRB paid a dividend of ₹2 last quarter while IndiaGrids paid a dividend of ₹3 last quarter, still, the latter is trading at ₹132/unit while IRB is trading at ₹75/Unit. (FV - Rs.100 for IndiaGrid and Rs.102 for IRB). The current quarterly yield of IRB is 1.7% more than IndiaGrid due to the additional risk.

Source: Nuvama Wealth

And lastly the order book and growth prospect. IRB has 5 major projects and 2 more to come. But out of these 5, some will be transferred to the government in the coming years. A lack of growth and lower cash flows in the short/medium term is one of the reasons that the price is low for IRB InvIT.

But even with all these arguments, the guidance for IRB InvIT seems to be an annual yield of 13-14% in the coming years. Thus, even with such a risk, and declining market price, one can argue that this might be a good investment opportunity.

But do remember, the yields only represent the periodic return on investments, the actual returns will be measured after taking into account the realizable value of the unit, ie. the gain or loss after selling the unit. Thus the actual return on IRB is likely to be less than that of IndiaGrids.

Asset-Backed - The investment is backed by cash-generating assets, thus lower risk.

Predictable and Consistent Cash Flows - Generally the cashflows are consistent and can be predicted. As 80% of the assets are revenue-generating, we have historical numbers about the performance of these infrastructure projects.

Lower Ticket Size - You can buy even 1 unit of any listed InvIT via your broker at the current market price just to get some exposure.

Regulated And Transparent - These products are regulated by SEBI, and InvITs are required to furnish their books of account 21 days before every quarter.

Direct way investing in Infra assets - InvIT is one of the few ways for retail investors to directly invest in huge infra projects providing some diversification compared to the traditional market.

Risk Of Cash Flows - As we saw in the previous example of IRB, cash flows may change depending upon various factors. This would not only result in less return on investment but also a lower realizable value of the unit.

Taxes - All the income generated is taxed as per the slab rates. There is hardly any tax exemption, thus making the post-tax return quite low and think about arguing with your CA on correct tax treatments of various forms of income from InvITs, it can be a nightmare.

Market Changes - Even though the macro factors do not affect the cash flow of the InvIT, they may affect the market price of the unit.

Research - A huge amount of research is required before investing in InvITs. As the returns are completely dependent on the assets chosen by the investment manager, one needs to study these assets and trust the investment manager to deliver the returns.

So finally, what do we think of this investment product and should you invest? At first, I thought the returns on InvITs would be lackluster, after all, how much can you expect from toll collection post operating expenses and taxes? But looking at various other options such as power grids, datacenters etc. the returns could be higher depending upon the type of InvIT you go for.

As a product though, one needs to do thorough research, as the performance of the InvIT completely depends upon the investment manager and the assets he has decided to invest in. And given how picky I am about my stocks, I would look at the background and history of investment managers, along with the assets of InvITs, their historical performance, valuation as compared to peers, new projects in the pipeline, expected future cash flows and also a complete industry/sector analysis.

So coming to whether to invest or not? It completely depends on your risk appetite and how much you love consistent cash flows. If you are someone who is into recurring payouts and slightly lower risk, this will be a good investment product for you. The only thing I would suggest to you is, to do your research properly before investing.

Thank you so much for reading, we are aware that InvITs are not a very common product and some people may not consider it as an alternative investment, however, we think otherwise given there are so many other unregulated fractional ownership structures coming up around these assets. Just because it's listed, doesn't mean we should ignore it.

We are on a mission to build out great content in alternative investment space in India, if you would like to join our Whatsapp Community where we regularly discuss ideas and clear doubts, please apply via the below link and if you want to watch this content in video format, do check out our Youtube channel.

Please note that this is an opinion blog and not official research advice. I am not a registered RIA in India, and none of these views reflect those of my current employer. This blog aims to promote informed decision-making and does not discourage you from investing in any deals.

We plan to come up with more blogs discussing different types of instruments available in the world of startup investing, write on due diligence for some platforms, and also existing and upcoming alt investment deals in the Indian market. If you want to stay updated on the latest blogs, please subscribe to our newsletter so you get notified automatically.

Thank you for reading and hope to see you in the next one!