KEY TAKEAWAYS

SEBI has introduced a 'Liquidity Window' facility to address the lack of liquidity in the corporate bond market, allowing investors to sell bonds back to issuers before maturity through a voluntary put option.

The liquidity window is optional for issuers and aims to attract more retail investors by providing a reliable exit option, enhancing the appeal of corporate bonds.

Key features include a minimum aggregate limit for the put option, designated stock exchanges for transactions, and specific eligibility criteria for retail investors.

The facility allows issuers to offer the liquidity window on a monthly or quarterly basis, with mechanisms in place to manage the volume of bonds sold back during each window.

While the initiative is seen as a potential game changer, questions remain about issuer incentives and the handling of defaults, with SEBI expected to provide further details in the future.

After introducing multiple ground-breaking announcements for the corporate bond market in the last couple of years, such as introduction of framework for OBPP platforms and reducing the minimum ticket size for debt securities investments from Rs 1 lakh to just Rs 10,000, India’s market regulator SEBI has come up with another big announcement for investors in the debt securities market, which is being seen as a potential game changer for bond investors.

SEBI Introduces ‘Liquidity Window’ Facility

Corporate Bonds are one of the best products in the alternative investment category, but even then they have not truly taken off and we recently conducted polls within our ALT Investor community where investors clearly choose lack of liquidity as one of the biggest turn offs when investing in bond market.

And now, in its latest circular dated 16th October 2024, SEBI has addressed this issue and introduced guidelines to put into place a framework for the introduction of a liquidity window facility by the issuers, for debt securities investors, through the voluntary put option. In SEBI’s own words they said:

One of the factors that drives investor participation in a market is the availability of liquidity. Low levels of secondary market transactions in corporate bonds (including due to a large number of institutional investors holding such bonds to maturity) has resulted in the corporate bond market being perceived as illiquid.

Maybe someone from SEBI is part of our community and monitoring our polls, you never know! By the way, you can check out SEBI’s full circular by clicking here.

What’s A Put Option?

Before we dig deeper into the circular and the liquidity window facility introduced by SEBI, let us help you understand what is a put option, if you don’t already know.

In simple words, through a put option, an investor purchases the right to or the option to sell back a bond before maturity, through a contract.

Let’s Take An Example

Suppose you bought a new car for Rs 5 Lakhs from a dealer. But you’re worried that the car’s resale value might drop significantly within the next one year. So, to protect yourself, you purchase a put option from the car dealership that guarantees you can sell the car back to them for Rs 400,000 within next one year, by paying a premium of Rs 10,000 for this put option.

Scenario 1: Car Value Drops: If the market value of your car drops to Rs 300,000 you can choose to exercise your put option and sell the car to the dealership, at the agreed upon price of Rs 400,000, hence minimizing your loss.

Scenario 2: Car Value Stays Stable: In case your Tata Motor car retains its value at Rs 500,000 and does not fall, you can choose to not exercise the put option. While in this case you would lose the Rs 10,000 premium paid, but still benefit from the car's retained value.

Also, for the unversed, premium is like the fee that the buyer pays to the seller for the right to buy or sell an underlying asset, usually such as stocks or bonds. In this case, premium will be the 1% penalty you will have to pay on the market yield when you are reselling the bond.

Why Has SEBI Introduced The Liquidity Window?

SEBI (Securities and Exchange Board of India) has introduced the Liquidity Window facility to address the perceived illiquidity in the corporate bond market. The facility aims to attract more investors, particularly the retail investors, by providing a mechanism for them to exit their investments on predetermined dates before maturity.

It’s fair to say that the corporate bond market in India faces challenges due to low levels of secondary market trading. Many institutional investors tend to hold bonds until maturity, leading to a perception of illiquidity and deterring potential investors, especially the retail ones.

So, SEBI’s introduction of liquidity window aims to tackle these issues by:

Improving liquidity: By offering a buyback option, the facility enhances the liquidity of corporate bonds, making them more appealing to investors who may need to access their funds before maturity.

Attracting retail investors: Retail investors, who are often more sensitive and concerned about the lack of liquidity in the debt securities market, are more likely to participate in the corporate bond market if they have a reliable exit option through this liquidity window.

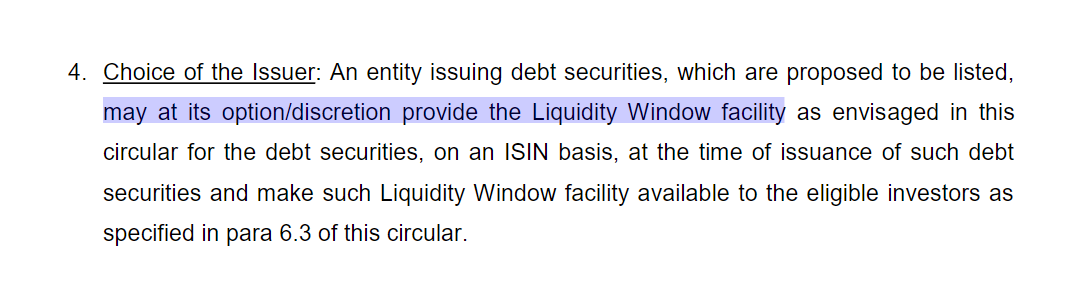

Is It A Mandatory Or Optional Facility?

The liquidity window facility is designed to be optional for issuers, as per SEBI circular.

Key Features Of The Liquidity Window

Minimum aggregate limit: Issuers must offer investors the option to exercise the ‘put option’ for at least 10% of the issue size.

Designated stock exchange: Issuers can select a designated stock exchange to facilitate the liquidity window, such as NSE or BSE.

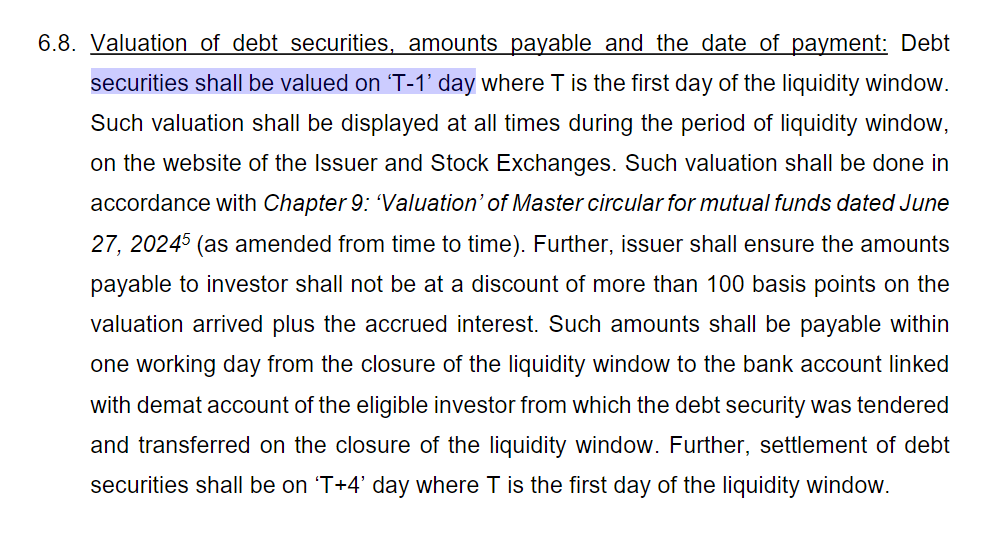

Valuation: Bonds are valued one day before the start of the liquidity window (T-1) using the valuation methodology specified in the SEBI Master Circular for mutual funds.

Issuers can opt for retail investor-specific window: SEBI requires the issuer to specify the eligibility of investors who can avail this liquidity window facility, i.e. whether the window shall be available to all investors in the debt securities market or only to retail investors. Here, the SEBI has specified that retail investors shall be those holders of non-convertible securities who have the aggregate face value of not more than Rs 2 lakh.

Issuance of facility: As per SEBI’s circular, the bond issuer can provide the liquidity window facility only after the expiry of one year from the date of the issuance of the debt securities.

Securities must be held in demat form: SEBI circular mentions that eligible investors who wish to avail the liquidity window facility must hold the debt securities in demat form.

- Settlement: Settlement of debt securities shall be on ‘T+4’ day basis, where T is the first day of the liquidity window.

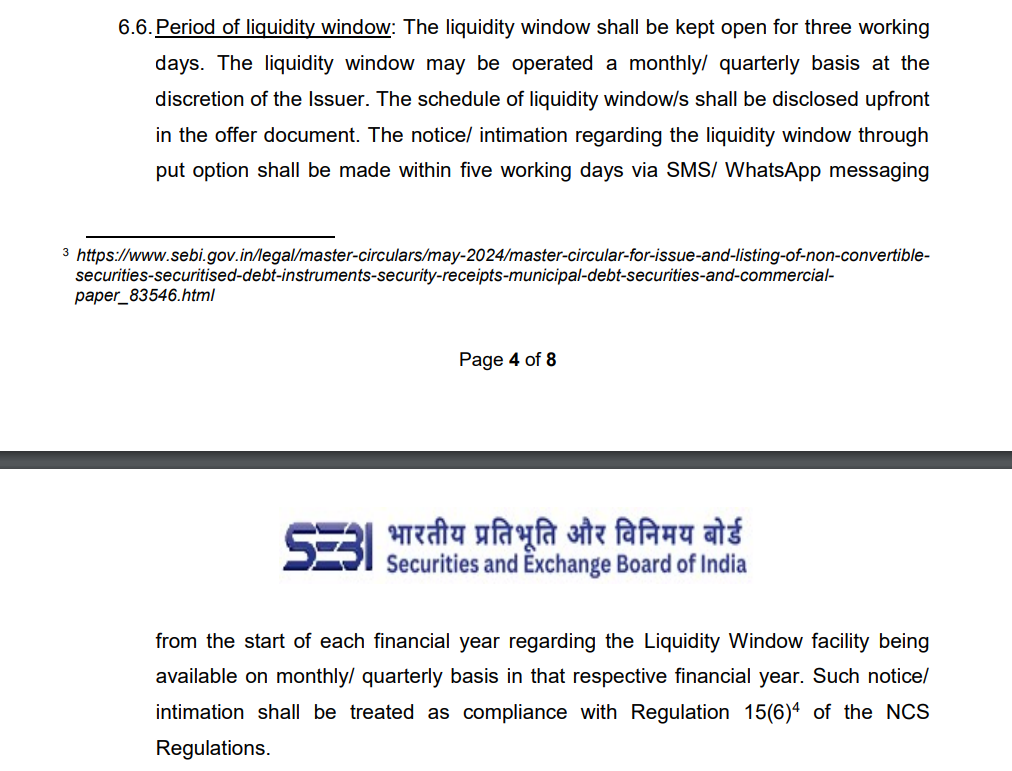

Frequency Of The Liquidity Window Facility

SEBI’s circular clearly gives issuers the flexibility to decide whether to offer this liquidity window facility on a monthly or quarterly basis.

The frequency of the liquidity window is expected to play a key role in an investor's strategy. For example, a more frequent liquid window such as a monthly one might be a really appealing option for investors who want to have their funds readily available with more liquidity. On the other hand, a quarterly liquidity window might be more suitable for investors with a longer term investment horizon.

What If Every Investor Rushes To Sell Bonds?

With the liquidity window in place, you may wonder that every investor can rush to sell their bonds, right? Well, SEBI has got that covered too, as the issuer of the bonds, i.e. the company that originally issued the bond, can put a limit on how many bonds can be sold back during each liquidity window. Moreover, they can also resell those bonds on the open market which helps to keep the market stable overall.

How Can The Liquidity Window Facility Be Availed?

SEBI’s circular further clarifies the mode and manner to exercise the put options under the liquidity window:

When the liquidity window opens, eligible investors can exercise the put option on debt securities by blocking the securities (such as bonds) in their demat account and utilizing the mechanism for notifying the exercise of put option to the issuer. Such exercise shall be done during trading hours. To be honest, we are not aware how this is done, but I am sure when the first bond is out, we will receive instructions.

Eligible investors may be permitted to modify or withdraw their bids during the liquidity window session.

All exercises of the put option on the debt securities received by the stock exchange until the end of trading hours on the date of closure of the liquidity window (i.e. day three of the Liquidity Window) and for which block is created, shall be treated as duly tendered.

What Will Issuer Do With The Bought Back Securities?

As per SEBI circular, the issuer may deal with the debt securities in either of the following ways, within 40-45 days of the closure of the liquidity window or before the end of the relevant quarter (whichever is earlier):

Sell such debt securities on the debt segment of stock exchange

Sell such debt securities directly on RFQ platform, if the Issuer is eligible to access the RFQ platform

Sell such debt securities through an Online Bond Platform

Extinguish such debt securities.

Possible Downsides Of The New Liquidity Window Facility?

While this initiative of introducing the liquidity window facility is being seen as a big and concrete step by the SEBI towards the growth of bond market, but a couple of questions crop up amidst the discussion around this decision.

Firstly, what is the incentive for the issuer to issue securities with a put option?

If an issuer expects their rating to improve or can get credit cheaper, buybacks through the put option are beneficial. The new SEBI regulation allows issuers to target specific investor groups, enabling partial rather than full buybacks. Issuers can also use this regulation if they can offer better pricing. SEBI allows repurchasing securities at up to a 1% discount from valuation plus interest, following their norms. This flexibility, along with options to resell or extinguish bonds, provides efficient debt management while supporting investor liquidity.

Second question that arises, is what happens if the issuer DEFAULTS and the put option which is essentially a right to sell cannot be exercised?

Well, that is where its important for you, as an investor, to always remember that the risk and possibility of an issuer defaulting always exists. At present, it does not seem pretty clear what regulations would surround the investor and issuer in case of latter’s default. SEBI might come up with further details on the same in future.

Conclusion

Now you may still be wondering, how effective can this liquidity window be, right? Well, since the liquidity window facility is a new initiative by SEBI, its effectiveness in addressing the challenges of the corporate bond market’s illiquidity remains to be seen.

One thing which I would like to make abundantly clear is that when the issuer buys back your security, the yield you will get is one percent less than the market yield on the T-1 basis.

However, by providing a clear framework, this facility seems to have the potential to boost investor confidence and encourage more participation in the market, possibly even becoming a game changer!

We will have to wait and see how bond market investors and issuers view this liquidity window and whether it can achieve its goal of solving liquidity issues in the bond market.

That's it for this one. I hope you found this article helpful, and got a fair understanding about this new liquidity window introduced by the SEBI. If you would like to join our exclusive spam-free WhatsApp community, you can apply here.

Please note that this is an opinion blog and not an official research or investment advice. This blog aims to help retail investors make an informed decision in the bond market, and neither encourages nor discourages you from investing in any particular bond or any other asset class.