Investing In BluSmart Assure: A 14% XIRR Asset Leasing Opportunity

KEY TAKEAWAYS

BluSmart Assure is an asset-leasing opportunity where investors purchase electric vehicles (EVs) and lease them to BluSmart, promising a 14% XIRR return over 48 months.

The investment requires a minimum commitment of ₹1.30 Crores for at least 10 cars, with BluSmart handling operational and maintenance expenses.

Investors can benefit from tax advantages and depreciation, but there are risks related to registration, insurance, and BluSmart's financial stability.

The deal involves fixed monthly lease rentals, but investors must manage GST invoicing and potential legal and credit risks.

While the deal offers attractive post-tax returns for high-net-worth individuals, it carries significant risks and is best suited for experienced investors.

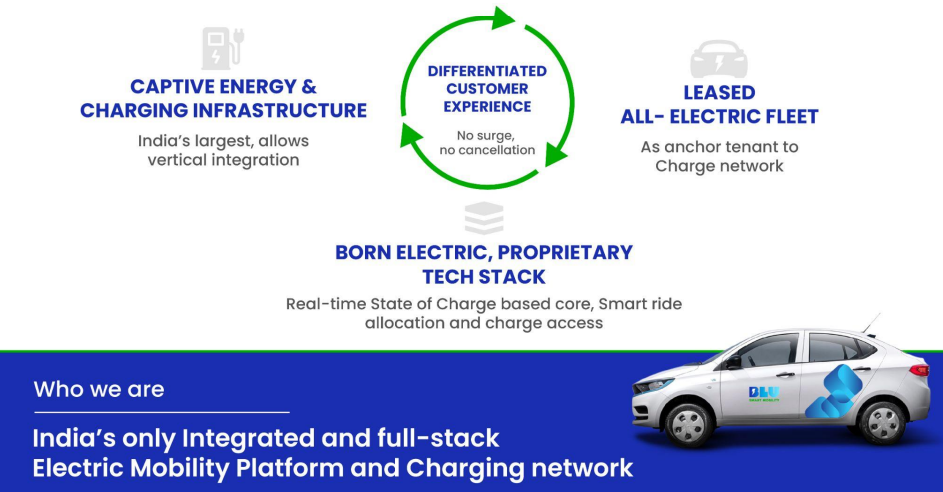

If you are from Delhi or Bangalore, you have likely seen the branded BluSmart cabs around the city, especially on routes to the airports. For those not from Delhi or Bangalore, BluSmart is a ride-hailing platform focused on Electric Vehicles (EV) and EV charging infrastructure. On the surface, BluSmart is just a taxi company like Ola and Uber, but at its core, the company is not just about ride-hailing. It is an energy, infrastructure, mobility, and tech company.

According to one of their founders, Punit Goyal, the company's core model is its EV charging infrastructure, while the ride-hailing business acts as an 'anchor tenant' using these charging stations to operate.

However, these charging infrastructures and EVs are costly, making the balance sheet heavy and creating a drag. With $200 million in debt and equity funding, and another $200 million in EV leases, a lot of cash has already been invested in the BluSmart ecosystem without a clear path to profitability. In fact, some experts have started to question the basic economics of their ride-hailing model.

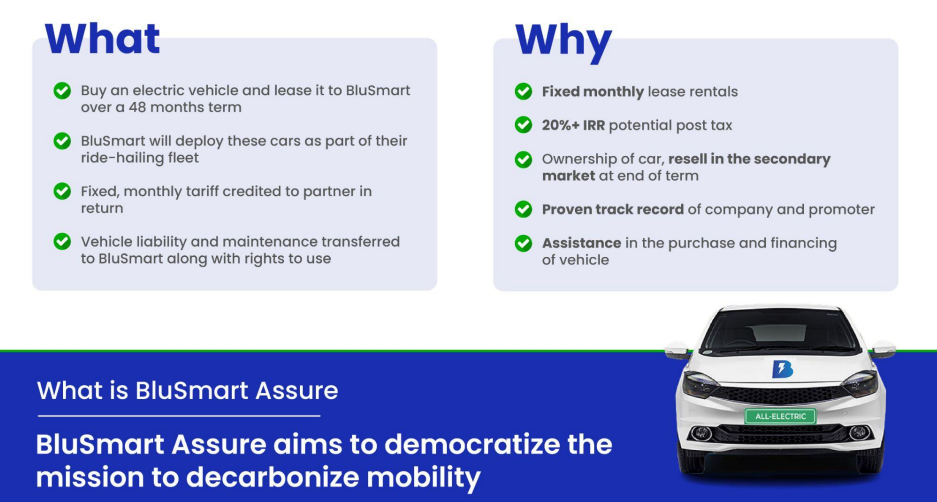

So, how can BluSmart expand further? One way is to raise more funds, which the company recently did in their May 2024 round. But this is an expensive method since it requires giving up valuable equity. In their ecosystem, the most expensive asset to purchase is the actual EV vehicle. So, BluSmart had an idea: why not crowdfund these vehicles from retail investors, corporates, and institutional investors? They call this program BluSmart Assure.

Assure is an asset-leasing deal where investors, typically high-net-worth individuals (HNIs), buy EVs and lease them to BluSmart to earn monthly lease rentals. BluSmart currently promises a 14% XIRR return over a 48-month period, with additional benefits like tax advantages and depreciation, though there are various risks involved.

We will dive into the details of the deal and how it works. But first, let's cover the basics.

We also have a very cool video discussing the EV Leasing market in India with Kunal Mundra (Founder & CEO, Electrifi Mobility), you can check it out here.

Quick Recap On Asset Leasing

Asset leasing is a straightforward investment structure where an investor buys an asset and rents it out to a third party in exchange for regular payments. We have explained the concept of asset leasing in detail in one of our previous article, including an analysis of a sample deal. We highly recommend you to read this article before you continue reading this one.

Specifics Of BluSmart Assure Deal

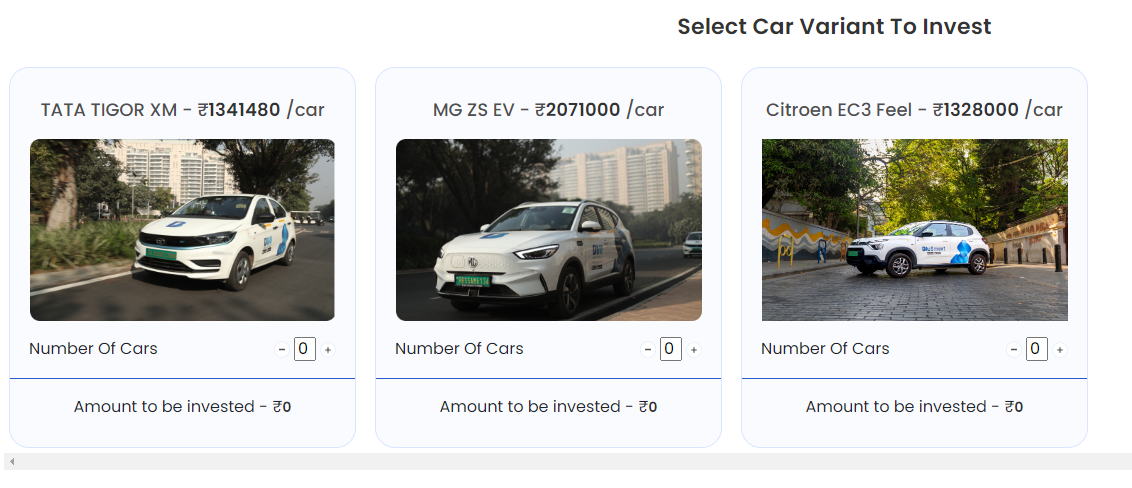

Blusmart Assure is a typical asset leasing deal wherein investors, such as HNIs, Businesses, Corporation etc. purchase EVs and lease it to BluSmart for a period of 4 years. We intentionally say HNIs because the this deal requires you to finance atleast 10 cars which will have an approx cost of ₹1.30 Crores.

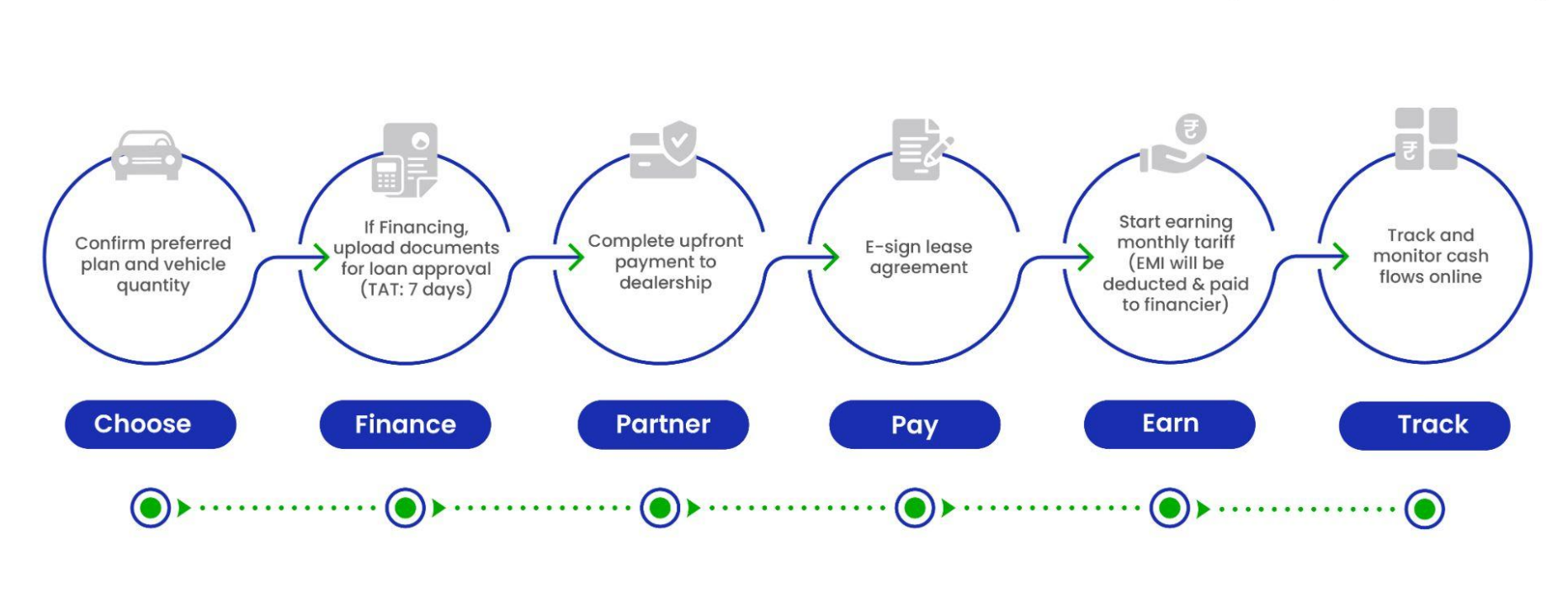

The investor can head to BluSmart Assure website, complete the formalities of KYC registration, signing the lease and service agreements, and then can go ahead with the purchase. BluSmart promises to help investors with dealership scouting, registration process, delivery, deployment and even financing.

But lets get into the specifics of what the deal is all about. While we had access to the agreement via our community members, we can't share it here due to its confidential nature. If you are interested in this deal and have the capacity to finance atleast 10 cars, you should be aware of the following points and then you can accordingly ask your questions to Blusmart team.

Registration

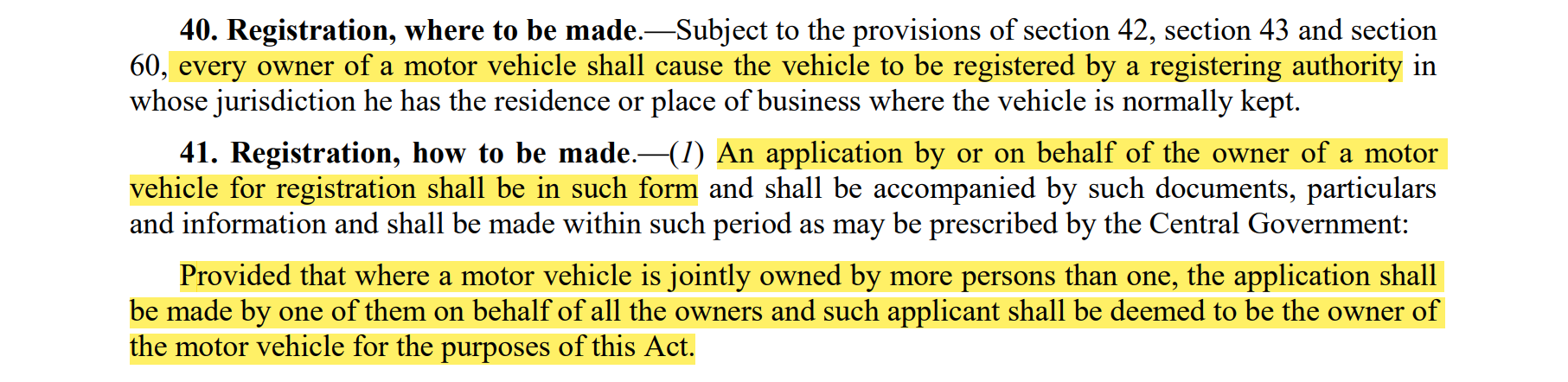

According to the terms set by BluSmart (Lessee), the cars will be registered in the name of BluSmart Mobility Private Limited during the purchase, and investors (Lessors) will only be the beneficial owners. We confirmed this with someone who has actually invested in this deal. The RC book they received listed BluSmart as the owner.

However, according to the Motor Vehicle Act 1988 (screenshot below), the registration should be done in the name of the owner, which is the investor in this case. There cannot be two different parties, one being the registered owner and one being the beneficial owner.

Now, I am sure BluSmart has a valid reason for registering the cars in their name. We couldn't find a satisfactory reason, but you should keep this in mind and ask them if needed.

Another point to note is that the cars will likely be registered in the state where BluSmart wants to operate them, not where the investor is from.

Insurance and Maintenance

Regarding insurance, BluSmart wants investors to pay for the first-year insurance fees, while they will cover the costs for the 2nd, 3rd, and 4th year. This increases the investment cost, as investors are already paying registration fees for the cars and service fees to BluSmart for managing the operations. This added cost will reduce your IRR, which BluSmart does not mention on its website.

During the 4 years, according to the agreements we reviewed, BluSmart promises to handle all operational and maintenance expenses, including major ones like battery replacements. In case of complete car damage, BluSmart will claim the insurance and reimburse the investors.

Billing and Lease Rentals

Once the cars are deployed, BluSmart will start paying monthly rentals, which will be visible on the investor dashboard on the website. However, the payment process is not automated. Investors will need to raise monthly lease rental invoices, including GST, and email them to the BluSmart team. This process becomes more hectic because you have to file GST on every invoice to offset your Input Tax Credit collected during the car purchase.

The good thing in this deal is that your payouts are fixed and not dependent on the miles driven by the car or the number of rides completed by the driver. Think of this arrangement as an asset-backed fixed income security, with fixed periodic payments.

Some Number Crunching

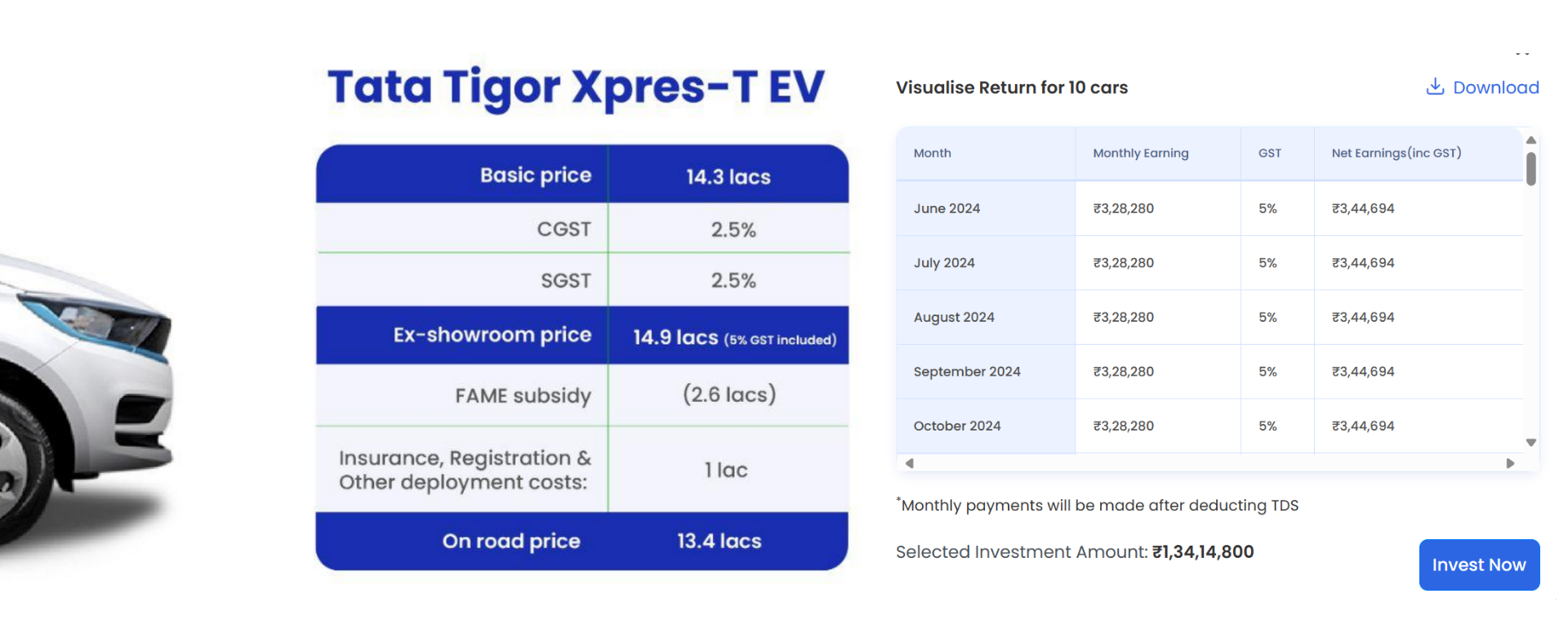

Let's understand the deal with the example of Tata Tigor EV, which costs anywhere between ₹13-14 lakhs on-road. As the minimum investment requirement of the deal is 10 cars, an investor will have to commit roughly ₹1.30 Cr. This number will be higher for MG cars and a bit lower for the Citroen cars.

The deal promises to provide investors a pre-tax IRR of 14%. Investors will receive a monthly payment of roughly ₹33,000 per car which translates to ₹3.3Lac for 10 cars. The buy-back value calculated by BluSmart is ₹1.2 Lakhs per car after 4 years. Some of you reading carefully will be surprised by such low buy-back number, but we will get to it later. The residual value is calculated as per the target IRR figure, and the math there adds up.

When summed up, investors will invest ₹1.35cr, and will receive ₹1.65cr (incl GST) at the end of 4 years. The returns don't seem to justify the effort behind the deal, but the twist is in the taxation and depreciation component.

Taxation and Depreciation

The biggest pull factor for this deal are the post tax returns. Being the owner of the car, investors can claim depreciation on the asset.And if you have financed the deal through a loan, you can also claim deductions on interest expenses. Note, you can only claim this if the loan is taken by a business and this is not applicable to salaried people. Please do consult a tax advisor before making any decisions.

Investors can charge depreciation upto 40% for the EVs on Written Down Value (WDV). If you are running a business, this depreciation expense can be subtracted from the profit to lower tax liability.

Assuming you setup a new SPV (LLP or Pvt Ltd.) just to make this investment and your only business income are these lease rentals, then you won't have any tax liability for the first 2 years because of the depreciation deductions, and the tax liability will decrease in 3rd and 4th year. The taxable component of the income will be taxed at company tax rate.

At the end of the tenure, if investor decides to sell the car back to BluSmart, you will be showing a loss in your books, as the book value of the asset is quite higher than the buyback value offered by BluSmart. This loss can again be used to adjust against your taxable income (if any). Surely a mouth-watering amount of savings when it comes to filing IT returns.

This deal does make a lot of sense with leverage (i.e. taking a loan to buy cars) and claiming depreciation and interest payment as deductions for tax benefits but if things go wrong, this same leverage can bite you back.

Risks In The BluSmart Assure Deal

One might ask, If everything is hunky-dory with the investment, then what is the catch? There are 2 big risks associated with this investment, which you should be aware of and comfortable with.

Contractual/Legal Risks

Motor vehicles are different from other leased assets like machinery or land. They have a specific and broad set of rules governing them.

We have reviewed the BluSmart lease and service contracts, and based on our analysis, there are several grey areas that may not favor retail investors. Since we can't share the actual agreement, here are some questions you should ask and check for yourself in the agreement to understand the risks:

Please click on every question to expand and read the answer.

Who bears any charges, duties or penalties by the government post the purchase and leasing of the car?

Can you really claim depreciation benefits if the car is actually not in your name but in Blusmart’s name?

Credit Risk / Default Risk

BluSmart has to pay the monthly lease rentals and buy back the car from its own pocket at the end of the tenure. So, its dependent upon 2 things to service the lease:

Net Revenue From Operations.

Funding Rounds in form of Equity or Debt.

But it is no surprise that BluSmart is high growth stage startup and is naturally bleeding money, with mounting losses and no clear defined path to profitability. So even though the charismatic founders of BluSmart can keep on raising money for the startup, the unit economics itself may not seem to make sense for a lot of investors (atleast for now)

The Morning Context did a good story on the Blusmart Assure model talking about the unit economics of this deal and Blusmart. You should check it out here:

Given the increasing lease rentals, the repayment burden will significantly increase for BluSmart in coming months and they will have to keep on raising more and more equity rounds to service this debt. Investors may stop funding them if there is no clear path to profitability.

All of this creates a big credit risk, which is hard to avoid. But the question is whether 14% XIRR is a good enough compensation for this kind of risk? I don't know about you, but it's not good enough for me.

Exit Risk

This is a weird one. The agreement we had access to states that the investor has an option to sell the vehicle post end of the lease term, but this provision is soon followed by the rights of BluSmart to invoke its Buy-Option, wherein investor has to compulsorily sell the vehicle to BluSmart at the residual value calculated by them at the beginning of the lease (If BluSmart decides to exercise their Buy-Option). There are two things not adding up here -

First is the residual value itself, which is calculated keeping in mind the XIRR figure of 14%. According to BluSmart, the residual value of each Tata Tigor car worth ₹13.5 Lakhs after 4 years is meagre ₹1.2 Lakhs. A WDV depreciation of 80%! If we go by the Income Tax rules, the depreciation charged on these assets are b/w 40-50%. And even according to market/reselling rates, these should be the ideal depreciation. Which means even though BluSmart is servicing the deal at 14% IRR, there is much more to gain for them than the investor.

So why give investor the option to sell the asset? Why not just structure the deal such that post the lease period, BluSmart will buyback all the cars for a fixed amount? It can be because, if the wear and tear is too high, or the fair value of car is less than the residual value, BluSmart may pass its option to buy-back.

Pros About This Deal

Post Tax Returns - These are attractive for high-net-worth individuals (HNIs). If an investor, who already runs a business, invests in this deal and opts for financing (i.e., taking a loan), the returns will be quite high. They can deduct depreciation and interest expenses to reduce their tax burden.

Asset-Backed - The investment is backed by assets. If the car gets damaged at any point, BluSmart will claim the insurance and pay it back to the investors.

Fixed Returns - The monthly lease rentals are fixed. As long as BluSmart is solvent, they will continue to pay the monthly lease rentals. However, in case of termination, only the pre-decided residual value for the period will be paid.

Backing by Good Institutional Investors - BluSmart has raised a significant amount of money from institutional venture capital players, which adds to their credibility. They have also secured vehicle financing from some big names. Although the terms and agreements for those deals might be different, it still enhances their credibility.

Cons About This Deal

Unfavorable Agreement Terms - As mentioned before, the lease agreement has many unfavorable terms or grey areas. In most cases, the investor will have to bear the liability or impact of these issues.

High Minimum Investment - The minimum investment of ₹1.3 Cr is quite steep, which reduces the investor base and excludes small business owners who might be interested in this opportunity.

Credit Risk - This is the biggest issue with the deal. The credit risk is quite high, as highlighted above. If a default occurs, you need to figure out how to take ownership of the physical asset, which may not be easy. We've seen similar challenges in other asset leasing defaults, such as the BigSpoon default on Grip Invest and the Growpital Leasing default on Tap Invest.

GST License - You need a GST license to enter into this arrangement with BluSmart. If you are an individual, this may be a lengthy and compliance-heavy process.

Conclusion

Now, should you invest? It depends on your needs and preferences. Given the high minimum investment and various operational and legal risks, I would place this product high on the risk spectrum.

However if you are too fixated on having some form of exposure in BluSmart, you can alternatively consider their Non-Convertible Debentures, which offer IRRs between 15-17% and have a tenure of max 1-2 years. Platforms like Tap Invest, Yubi, and Finzace are actively selling these.

This Blusmart Assure option is suitable for those who want asset-backed, high post-tax, fixed monthly returns. However, to achieve this, investors must take on significant risk and handle a lot of paperwork. Therefore, it is better suited for High Net Worth Individuals (HNIs) who are experienced and understand what they are getting into.

That being said, many people have invested in this deal, indicating there is a market for it. If you are considering investing, weigh the risks and rewards, consult your CA to understand the depreciation and financing benefits, and start earning those monthly rentals.

Thank you for reading this article so far. We are on a mission to build out great content and community in alternative investment space in India, if you would like to join our Whatsapp Community where we regularly discuss ideas and clear doubts, please apply via the below link.

Please note that this is an opinion blog and not official research advice. I am not a registered RIA in India, and none of these views reflect those of my current employer. This blog aims to promote informed decision-making and does not discourage you from investing in any deals.

We plan to come up with more blogs discussing different types of instruments available in the world of startup investing, write on due diligence for some platforms, and also existing and upcoming alt investment deals in the Indian market. If you want to stay updated on the latest blogs, please subscribe to our newsletter so you get notified automatically.

Thank you for reading and hope to see you in the next one!